The Role of Commercial Banks in the Economy and the 7 Characteristics of Insurable Risks

- The role of banks in the economy has been a subject of debate for many decades now. Some argue that bank are very relevant and they play significant roles in the economy while others believe that they are more interested in reaping off the masses through exorbitant charges on the service they provide. What is your opinion on this matter?

2. What do you understand by the 7 Characteristics of insurable risks? Which of the characteristics do you consider most important or least important?

Name: Ezeamaku Chukwuemeka Victor

Reg no: 2017/243370

Dept: Economics

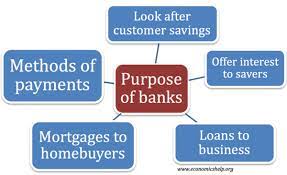

Functions of commercial banks

1)Accepting deposits: The traditional function of the central bank is the acceptance and safe keeping of deposits.

2)Provision of loans: Commercial banks give out loans to the public.

3)Transfer of funds/payment: They enable transfer of money from one party to another.

4)Credit Creation: Commercial banks create credit through accepting deposits and providing loans.

5)Agency functions: Commercial banks act as agents to the banking system and their customers.

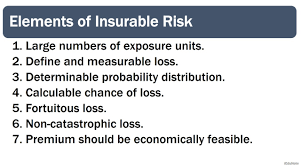

There are 7 Elements of insurable Risks:

1.Large numbers of exposure units.

2. Define and measurable loss.

3. Determinable probability distribution.

4. Calculable chance of loss.

5. Fortuitous loss.

6. Non-catastrophic loss.

7. Premium should be economically

The calculable chance of loss is the one I view as being most important

Name:Eze Udoka Chidiebube

Reg no:2017/242428

Dept:Economics

A vital component of the banking system is the commercial bank.We’ll be taking a look at what commercial banks are; and why they’re so important.

Functions of Commercial Banks in Nigeria

Commercial banks carry out several activities. Their most prominent roles are;

Accepting deposits: Commercial banks are mostly recognized for one essential function; accepting deposits from the general public. It is the most traditional function of all. There are three types of deposits — savings, current, and fixed. Existing account holders can withdraw their cash whenever they choose at their convenience. Savings accounts operate on a longer termed basis and attract interests because the deposits are investments. Fixed deposit accounts, on the other hand, work on a set period, and draw a fixed interest rate. See how to calculate the fixed deposit interest rate in Nigeria.

Provision of loans: besides accepting deposits, another function of commercial banks is the provision of loans. The provision of funds to those who require them for transactions is a vital role commercial banks play. Nowadays, customers can now have access to instant loans from commercial banks.

Transfer of funds: the transfer of funds from a customer’s account to another account is another vital function of banks. Fund transfer is a valid means of paying for transactions, as well as other financial activities. Transfer of funds can be carried out through several ways such as drafts, standing orders, cheques, USSD platforms, and electronic banking.

Credit Creation: commercial banks are perhaps the only financial institutions with this unique function. Commercial banks create credit through accepting deposits and providing loans — pushing money into the economy.

Agency functions: commercial banks are already agents of the banking system, but they can also be personal agents to their customers. An agent is an individual or institution that carries out activities, in this case, financial operations, on behalf of the principal (who is the customer) for a few known as a commission.

There are ideally seven characteristics of an insurable risk:

A.There must be a large number of exposure units.

B.The loss must be accidental and unintentional.

C.The loss must be determinable and measurable.

D.The loss should not be catastrophic.

E.The chance of loss must be calculable.

F.The premium must be economically feasible.

G.Fortuitous loss

Reg no: 2017/249521

Dept: Economics

What Is a Commercial Bank?

The term commercial bank refers to a financial institution that accepts deposits, offers checking account services, makes various loans, and offers basic financial products like certificates of deposit (CDs) and savings accounts to individuals and small businesses. A commercial bank is where most people do their banking.

Commercial banks make money by providing and earning interest from loans such as mortgages, auto loans, business loans, and personal loans. Customer deposits provide banks with the capital to make these loan.

THE ROLE OF COMMERCIAL BANK IN THE ECONOMY:

Commercial banks are crucial to the fractional reserve banking system, currently found in most developed countries. This allows banks to extend new loans of up to (typically) 90% of the deposits they have on hand, theoretically growing the economy by freeing capital for lending.

7 CHARACTERISTICS OF INSURABLE RISK

Insurance is a device that gives protection against risk. But not all both individual and commercial risks can be insured and given protection.

A risk must have certain elements or fcdtors in it that make it insurable. For pure risks to be insurable, it should possess the following characteristics.

Insurance providers look for these to measure levels of risk and levels of the premium for insurance protection for anything.

I.Large numbers of exposure units.

II.Define and measurable loss.

III.Determinable probability distribution.

IV.Calculable chance of loss.

V.Fortuitous loss.

VI.Non-catastrophic loss.

VII.Premium should be economically feasible.

VII.These are explained below;

1. Large Numbers of Exposure Units

The theory of insurance is based on the law of large numbers.

Therefore the prime necessity for a risk to be insurable is that there must be a sufficiently large number of homogeneous exposures to combine reasonably predictable losses.

Lost data can be compiled over time, and losses for the group as a whole can be predicted with some accuracy. The loss costs can then be spread over all insured’s in the underwriting class.

Also, the probabilistic estimates used by the insurance company, by logic, assume a large number of units in a distribution and insurance products are priced accordingly.

2. Define and Measurable Loss

A second requirement is that the loss should be both determinable and measurable. This means the loss should be definite as to cause, time, place, and amount. Life insurance is most cases meets this requirement easily.

The cause and time of death can be readily determined in most cases, and if the person is insured, the face amount of the life insurance policy is the amount paid.

The losses are fairly predictable and can be measured in money terms. Loss of peace of mind, tension, etc. Or loss of life cannot be indemnified.

3. Determinable Probability Distribution

The probability distribution of happening of an adverse event if determinable. This condition is necessary to establish a free premium according to the theory of equivalence.

If there is not determinable distribution, there is no question of issuing a cover by an insurance company.

4. Calculable Chance of Loss

A fourth requirement is that the chance of loss should be calculable. The insurer must be able to calculate both the average frequency and the average severity of future losses with some accuracy.

This requirement is necessary so that a proper premium can be charged that is sufficient to pay all claims and expenses and yield a profit during the policy period.

Certain losses, however, are difficult to insure because the chance of loss cannot be accurately estimated, and the potential for a catastrophic loss is present.

Example: floods, wars, and cyclical unemployment occur on an irregular basis, and prediction of the average frequency and the severity of losses are difficult.

Thus, without government assistance, these losses are difficult for private companies to insure.

5. Fortuitous Loss

The adverse event may or may not occur in the future and once the insurance company has no control. Naturally, if the event is non-random or the loss has occurred in the past, there is no question of insurance.

Also, it is important to note that randomness is ensured by underwriters who guard against adverse selection; the tendency of the poorer than average insured to seek or continue insurance coverage.

6. Non-catastrophic Loss

The losses should be non-catastrophic. Not all the units in a homogeneous group will be subject to an adverse event. This means that a large proportion of exposure units should not incur losses at the same time.

As we stated earlier, pooling is the essence of insurance. If most or all of the exposure units in a certain class simultaneously incur a loss, then the pooling technique breaks down and becomes unworkable.

Premiums must be increased to prohibitive levels, and the insurance technique is so long a viable arrangement by which losses of the few are spread over the entire group.

Example: insurers ideally wish to avoid all catastrophic losses.

In reality, however, this is impossible, because catastrophic losses periodically result from floods, hurricanes, tornadoes, earthquakes, forest fires, and other natural disasters. Catastrophic losses can also result from acts of terrorism.

7. Premium Should be Economically Feasible

It is the final requirement that the premium should be economically feasible. The insured must be able to pay the premium.

Also, for the insurance to be an attractive purchase, the premiums paid must be substantially less than the face value, or amount, of the policy.

Since the insurance pool is structured to be sufficiently large, the price charged by the insurer for buying the risk is generally low. It should be sufficient to cause the rich for the insurer as well as viable for the insured.

NAME: MBAH CHIEBONAM

REG NO: 2017/249525

DEPT: ECONOMICS

Question 1

A. Mobilizing Savings for Capital Formation: Commercial Bank helps to mobilize dormant savings and to make them available to the entrepreneurs for productive purposes, the development of a sound system of commercial banking is essential.

B. Existence of a Large Non-monetized Sector:

A developing economy such as Nigeria is characterized by the existence of a large non-monetized sector, particularly, in the backward and inaccessible areas of the country. The existence of this non-monetized sector is a hindrance in the economic development of the country. The banks by opening branches in rural and backward areas can promote the process of monetization in the economy.

C .Financing Industrial Sector:

Commercial Banks provide short-term and medium- term loans in the industry. In Nigeria, they undertake financing of small scale industries and also provide hire-purchase finance. These banks not only provide finance for industry but also help in developing the capital market which is underdeveloped in such countries.

D. Commercial Banks Help in Monetary Policy: By following the monetary policy of the Central Bank. The Central Bank is dependent upon those Commercial Banks for the success of the monetary management in keeping with requirements of a developing economy.

E.They Help in Financing Internal and External Trade:The banks provide loans to wholesalers and retailers to stock goods in which they deal. They also help in the movement of goods from one place to another by providing all types of facilities such as discounting and accepting bills of exchange, providing overdraft facilities, issuing drafts etc. They help by giving finance both exports and imports of developing countries such as Nigeria.

F. Need for Sound Banking System:

In developing countries, there should be proper facility of cheap remittance facilities to enable the movement of funds from one place to another, so as to meet the requirements of trade and industry. Also It should always be remembered that in developing countries loans should be given for productive purposes only and not for consumption and speculative purposes.It will be better and encouraging if long-term credit is given to agriculture and small scale industries.

Question 2

Private insurers generally insure only pure risks. However, some pure risks are not privately insurable. From the viewpoint of a private insurer, an insurable risk ideally should have certain characteristics. There are ideally six characteristics of an insurable risk:

• There must be a large number of exposure units.

• The loss must be accidental and unintentional.

• The loss must be determinable and measurable.

• The loss should not be catastrophic.

• The chance of loss must be calculable.

• The premium must be economically feasible

Name: Anayo Bright Udochukwu

Reg Number: 2017/249482

Department: Economics

1. Considering the role of banks in the economy . Some argue that bank are very relevant and they play significant roles in the economy while others believe that they are more interested in reaping off the masses through exorbitant charges on the service they provide.

The truth of the matter is that the commercial banks and the very other banks have been helping in intermediation of the economy in one way or the other. At least, through asset security and finacial wise. However, the issue concerning the interest is matter of thought because it is one of their source of income. Though, the central bank of any country should be able to courtil high interest rate set by its commercial banks.

2. What i understand by insurable risks are accidental occurence which a private or government set aside organisation can take up the responsibility so that individuals who by either means got affected based on any of their insured asset(s) cannot they the full responsibility alone.

However the risk i find much important is the accidental risks. Thus, it is good to know that accident occurs every now and then.

Name: Abiazia Rufus Chidiebube

Reg: 2017/243371

Dept: Economics

1.The role of commercial bank as great as it is, but there are certain elements that made it something to ask why should someone save his money in the bank.

Commercial bank in Nigeria issues huge charge in the cause of maintenance.

They accept deposit at all time and denies withdrawal, running business with a depositors’ fund with no or little interest to the depositor.

The activities of commercial Banks are not balance, at beat they are after securing the bank from risk thank than individuals fund.

2. That before any insurance to a particular risk it must fulfil this 7 condition, for it to be insurable. I considered The premium should be economically feasible to be the most important characteristics: it means that charge that an insured is to pay is to be moderate, there should be a Pareto efficient ( everyone to be better off). That’s the marginal cost of pay the premium should be equal to marginal benefit if the risk occurred

NAME: MGBADA OGOCHUKWU EMELDA

REG NO:2017/245040

DEPARTMENT: ECONOMICS

COMMERCIAL BANK

The term commercial bank refers to a financial institution that accepts deposits, offers checking account services, makes various loans, and offers basic financial products like certificates of deposit (CDs) and savings accounts to individuals and small businesses. A commercial bank is where most people do their banking. Commercial banks make money by providing and earning interest from loans such as mortgages, auto loans, business loans, and personal loans. Customer deposits provide banks with the capital to make these loans.

Major risks for banks include credit, operational, market, and liquidity risk. Since banks are exposed to a variety of risks, they have well-constructed risk management infrastructures and are required to follow government regulations. Government agencies, such as the Office of Superintendent of Financial Institutions (OSFI) in Canada, set the regulations to counteract risks and protect depositors.

Credit Risk

Credit risk is the biggest risk for banks. It occurs when borrowers or counterparties fail to meet contractual obligations. An example is when borrowers default on a principal or interest payment of a loan. Defaults can occur on mortgages, credit cards, and fixed income securities. Failure to meet obligational contracts can also occur in areas such as derivatives and guarantees provided.

While banks cannot be fully protected from credit risk due to the nature of their business model, they can lower their exposure in several ways. Since deterioration in an industry or issuer is often unpredictable, banks lower their exposure through diversification.

By doing so, during a credit downturn, banks are less likely to be overexposed to a category with large losses. To lower their risk exposure, they can loan money to people with good credit histories, transact with high-quality counterparties, or own collateral to back up the loans.

Operational Risk

Operational risk is the risk of loss due to errors, interruptions, or damages caused by people, systems, or processes. The operational type of risk is low for simple business operations such as retail banking and asset management, and higher for operations such as sales and trading. Losses that occur due to human error include internal fraud or mistakes made during transactions. An example is when a teller accidentally gives an extra $50 bill to a customer.

On a larger scale, fraud can occur through the breaching a bank’s cybersecurity. It allows hackers to steal customer information and money from the bank, and blackmail the institutions for additional money. In such a situation, banks lose capital and trust from customers. Damage to the bank’s reputation can make it more difficult to attract deposits or business in the future.

Market Risk

Market risk mostly occurs from a bank’s activities in capital markets. It is due to the unpredictability of equity markets, commodity prices, interest rates, and credit spreads. Banks are more exposed if they are heavily involved in investing in capital markets or sales and trading.

Commodity prices also play a role because a bank may be invested in companies that produce commodities. As the value of the commodity changes, so does the value of the company and the value of the investment. Changes in commodity prices are caused by supply and demand shifts that are often hard to predict. So, to decrease market risk, diversification of investments is important. Other ways banks reduce their investment include hedging their investments with other, inversely related investments.

Liquidity Risk

Liquidity risk refers to the ability of a bank to access cash to meet funding obligations. Obligations include allowing customers to take out their deposits. The inability to provide cash in a timely manner to customers can result in a snowball effect. If a bank delays providing cash for a few of their customer for a day, other depositors may rush to take out their deposits as they lose confidence in the bank. This further lowers the bank’s ability to provide funds and leads to a bank run.

Reasons that banks face liquidity problems include over-reliance on short-term sources of funds, having a balance sheet concentrated in illiquid assets, and loss of confidence in the bank on the part of customers. Mismanagement of asset-liability duration can also cause funding difficulties. This occurs when a bank has many short term liabilities and not enough short-term assets.

Short-term liabilities are customer deposits or short-term guaranteed investment contracts (GICs) that the bank needs to pay out to customers. If all or most of a bank’s assets are tied up in long-term loans or investments, the bank may face a mismatch in asset-liability duration.

Regulations exist to lessen liquidity problems. They include a requirement for banks to hold enough liquid assets to survive for a period of time even without the inflow of outside funds.

Many banks operate under the false pretense that because they are deemed a “conservative bank,” there isn’t a lot of risk in their business model. I often remind boards of directors that they sit on a highly leveraged, regulated hedge fund. Would they lend money to a finance company leveraged 10 times or more, while trying to manage a 3.5 percent spread? That’s your average bank. So it might be a good idea to consider an opportunity to reduce risk, even by an incremental amount.

The first thing to do is identify the area with the greatest risk. Most banks view it as credit risk, and vigorously address this with underwriting, loan committee, loan reviews, regulatory exams, reserves, limits and diversification. Banks do a great job of this. However, in our experience, the greatest area of risk, receiving the least amount of attention, is a bank’s “bond-like risk,” which shows up in the structure of securities, loans and deposits.

This risk is basically interest rate risk, and the devil is in such details as yield curves, repricing risk and maturities. While asset/liability management strategies may help, they don’t reduce the problem banks have with their dependence on duration (which is the measurement of the sensitivity of a bond to interest rate fluctuations) in exchange for a decent return. Over 80 percent of risk factor contribution to the price volatility on a bank’s balance sheet is caused by nominal duration. What this means is loans, securities and deposits all have the same structured risk which is caused by maturities and cash flows. In light of this enormous risk concentration, pension funds, endowments, foundations and other institutions diversify this risk via stock and private equity allocations. For example, private equity allocations can reduce risk and increase returns through:

• Lower volatility of returns over time compared to duration-based assets like loans and bonds. Yes, private equity has a lower volatility risk than a two-year Treasury note.

• Higher Sharpe Ratios than bonds or loans, which means higher returns per unit of risk. (William F. Sharpe first introduced returns-based style analysis in the late 1980s, hence the name “Sharpe Ratio.”)

• Very low correlation coefficients to bonds and loans, meaning the returns don’t track those of bonds or loans which will help your bank diversify its earnings stream. Banks currently try to do this through non-interest income.

• Economic cycle diversification benefits for banks that can only lend money even when pressed by market forces on pricing and structure. Private equity mitigates this by investing in different parts of the capital structure than loans, and by less stringent investing periods than banks. Banks need to lend or invest their depositors’ funds immediately. Private equity funds can be more patient because they typically have a three- to five-year window in which to put their investors’ money to work.

Banks aren’t allowed to invest in private equity funds, so why am I telling you this? While banks are prohibited from investing in private equity funds, there is an exception in the Dodd-Frank Act’s Volcker Rule for Small Business Investment Companies (SBICs), which are funds that invest in small businesses and private companies. Hundreds of banks have taken advantage of this program since 1958. There are several benefits to these investment vehicles. Banks can:

• Help create jobs and expand the economy.

• Get Community Reinvestment Act (CRA) credit.

• Get CRA service credit by serving on an advisory board.

• Create opportunities for senior C&I loans.

• Create opportunities for commercial deposits.

• Offer solutions to customers who need a liquidity event, more equity in their business or support for a senior loan.

• Earn a nice return.

SBICs, like private equity, also help reduce the aforementioned risks of volatility, duration, correlations, Sharpe Ratios, economic cycle timing and diversification, which theoretically should increase portfolio returns. SBICs can make a bank safer and more profitable. Top quartile returns (returns in the top 25 percent) for SBICs from 1998 to 2010 were higher than 15 percent, while even the bottom quartile was 6.3 percent. So even a poor performing SBIC has produced higher returns than most any other asset opportunity available to a bank during this time frame. To reduce the risk of investing in a poor performing SBIC, a bank can do the following:

1. Develop underwriting practices, like a bank does on loans, tailored to SBICs, targeting top quartile returns.

2. Create a portfolio of multiple SBICs based on the 5 percent capital limit for bank investments to diversify company and fund manager exposure.

3. Seek the advice of financial advisory firm.

Being conservative doesn’t mean not doing anything new, it means constantly trying to find ways to decrease risk. Any time one can reduce risk and increase profitability, it should be strongly evaluated.

NAME: MGBADA OGOCHUKWU EMELDA

REG NO:2017/245040

DEPARTMENT: ECONOMICS

THE ROLE OF COMMERCIAL BANKS IN ECONOMY

The banking system is a catalyst and engine of growth that is responsible for being a lifewire to every sector of the economy. It is evident that no sector in the economy can flourish or prosper without the support and services of the banking sector, agricultural sector, manufacturing sector, mining or even services sector can’t do without banks. Commercial banks provide and encourage savings. The establishment of commercial bank especially in the rural areas makes savings possible, hence economic development is accelerated.

Commercial banks provide capital needed for development. Deficit spender unit obtain medium and short term loans and overdraft from commercial banks to start a new industry or to engage in other development efforts. They engage in trade activities through making use of cheques and other financial instrument possible. They encourage investment, provide direct loans to the government and individuals for investment purposes. They provide managerial advices to small-scale industrialists who do not engage in the service of specialist. Commercial banks also render financial advice to their customers including to invest in. Commercial banks create money as an instrument to the apex bank for all its activities. Commercial banks help to enhance development of international trade, these include acting as referees to importers, providing travellers cheque to those going abroad, opening letters of credit as well as providing credit for export. All these helps to promote international trade and relationship between nations, they provide backup liquidity to the economy. They are transmitters of monetary policy and they provide some “value added” from transfering funds from savers to borrowers and providing liquidity.

Role of Commercial Banks

• Mobilising Saving for Capital Formation: …

• Financing Industry: …

• Financing Trade: …

• Financing Agriculture: …

• Financing Consumer Activities: …

• Financing Employment Generating Activities: …

• Help in Monetary Policy:

INSURABLE RISK;A risk that conforms to the norms and specifications of the insurance policy in such a way that the criterion for insurance is fulfilled is called insurable.

CHARACTERISTICS OF INSURABLE RISK

• Large number of similar exposure units. …

• Definite Loss. …

• Accidental Loss. …

• Large Loss. …

• Affordable Premium. …

• Calculable Loss. …

• Limited risk of catastrophically large losses.

Insurance companies normally only indemnify against pure risks, otherwise known as event risks. A pure risk includes any uncertain situation where the opportunity for loss is present and the opportunity for financial gain is absent.

Speculative risks are those that might produce a profit or loss, namely business ventures or gambling transactions. Speculative risks lack the core elements of insurability and are almost never insured.

Examples of pure risks include natural events, such as fires or floods, or other accidents, such as an automobile crash or an athlete seriously injuring his or her knee. Most pure risks can be divided into three categories: personal risks that affect the income-earning power of the insured person, property risks, and liability risks that cover losses resulting from social interactions. Not all pure risks are covered by private insurers.

Due to Chance

An insurable risk must have the prospect of accidental loss, meaning that the loss must be the result of an unintended action and must be unexpected in its exact timing and impact.

The insurance industry normally refers to this as “due to chance.” Insurers only pay out claims for loss events brought about through accidental means, though this definition may vary from state to state. It protects against intentional acts of loss, such as a landlord burning down his or her own building.

Definiteness and Measurability

For a loss to be covered, the policyholder must be able to demonstrate a definite proof of loss, normally in the form of bills in a measurable amount. If the extent of the loss cannot be calculated or cannot be fully identified, then it is not insured. Without this information, an insurance company can neither produce a reasonable benefit amount or premium cost.

IJIGA CHRISTIAN ADAKOLE

2017/241255

EDUCATION/ECONOMICS

TOPIC: THE ROLE OF COMMERCIAL BANK IN THE ECONOMY (INSURABLE RISK).

The main functions of commercial banks are accepting deposits from the public and advancing them loans.

However, besides these functions there are many other functions which these banks perform. All these functions can be divided under the following heads:

1. Accepting deposits

2. Giving loans

3. Overdraft

4. Discounting of Bills of Exchange

5. Investment of Funds

ADVERTISEMENTS:

6. Agency Functions

7. Miscellaneous Functions

1. Accepting Deposits:

The most important function of commercial banks is to accept deposits from the public. Various sections of society, according to their needs and economic condition, deposit their savings with the banks.

ADVERTISEMENTS:

For example, fixed and low income group people deposit their savings in small amounts from the points of view of security, income and saving promotion. On the other hand, traders and businessmen deposit their savings in the banks for the convenience of payment.

Therefore, keeping the needs and interests of various sections of society, banks formulate various deposit schemes. Generally, there ire three types of deposits which are as follows:

(i) Current Deposits:

The depositors of such deposits can withdraw and deposit money whenever they desire. Since banks have to keep the deposited amount of such accounts in cash always, they carry either no interest or very low rate of interest. These deposits are called as Demand Deposits because these can be demanded or withdrawn by the depositors at any time they want.

ADVERTISEMENTS:

Such deposit accounts are highly useful for traders and big business firms because they have to make payments and accept payments many times in a day.

(ii) Fixed Deposits:

These are the deposits which are deposited for a definite period of time. This period is generally not less than one year and, therefore, these are called as long term deposits. These deposits cannot be withdrawn before the expiry of the stipulated time and, therefore, these are also called as time deposits.

These deposits generally carry a higher rate of interest because banks can use these deposits for a definite time without having the fear of being withdrawn.

ADVERTISEMENTS:

(iii) Saving Deposits:

In such deposits, money upto a certain limit can be deposited and withdrawn once or twice in a week. On such deposits, the rate of interest is very less. As is evident from the name of such deposits their main objective is to mobilise small savings in the form of deposits. These deposits are generally done by salaried people and the people who have fixed and less income.

2. Giving Loans:

The second important function of commercial banks is to advance loans to its customers. Banks charge interest from the borrowers and this is the main source of their income.

Banks advance loans not only on the basis of the deposits of the public rather they also advance loans on the basis of depositing the money in the accounts of borrowers. In other words, they create loans out of deposits and deposits out of loans. This is called as credit creation by commercial banks.

Modern banks give mostly secured loans for productive purposes. In other words, at the time of advancing loans, they demand proper security or collateral. Generally, the value of security or collateral is equal to the amount of loan. This is done mainly with a view to recover the loan money by selling the security in the event of non-refund of the loan.

At limes, banks give loan on the basis of personal security also. Therefore, such loans are called as unsecured loan. Banks generally give following types of loans and advances:

(i) Cash Credit:

In this type of credit scheme, banks advance loans to its customers on the basis of bonds, inventories and other approved securities. Under this scheme, banks enter into an agreement with its customers to which money can be withdrawn many times during a year. Under this set up banks open accounts of their customers and deposit the loan money. With this type of loan, credit is created.

(iii) Demand loans:

These are such loans that can be recalled on demand by the banks. The entire loan amount is paid in lump sum by crediting it to the loan account of the borrower, and thus entire loan becomes chargeable to interest with immediate effect.

(iv) Short-term loan:

These loans may be given as personal loans, loans to finance working capital or as priority sector advances. These are made against some security and entire loan amount is transferred to the loan account of the borrower.

3. Over-Draft:

Banks advance loans to its customer’s upto a certain amount through over-drafts, if there are no deposits in the current account. For this banks demand a security from the customers and charge very high rate of interest.

4. Discounting of Bills of Exchange:

This is the most prevalent and important method of advancing loans to the traders for short-term purposes. Under this system, banks advance loans to the traders and business firms by discounting their bills. In this way, businessmen get loans on the basis of their bills of exchange before the time of their maturity.

5. Investment of Funds:

The banks invest their surplus funds in three types of securities—Government securities, other approved securities and other securities. Government securities include both, central and state governments, such as treasury bills, national savings certificate etc.

Other securities include securities of state associated bodies like electricity boards, housing boards, debentures of Land Development Banks units of UTI, shares of Regional Rural banks etc.

6. Agency Functions:

Banks function in the form of agents and representatives of their customers. Customers give their consent for performing such functions. The important functions of these types are as follows:

(i) Banks collect cheques, drafts, bills of exchange and dividends of the shares for their customers.

(ii) Banks make payment for their clients and at times accept the bills of exchange: of their customers for which payment is made at the fixed time.

(iii) Banks pay insurance premium of their customers. Besides this, they also deposit loan installments, income-tax, interest etc. as per directions.

(iv) Banks purchase and sell securities, shares and debentures on behalf of their customers.

(v) Banks arrange to send money from one place to another for the convenience of their customers.

7. Miscellaneous Functions:

Besides the functions mentioned above, banks perform many other functions of general utility which are as follows:

(i) Banks make arrangement of lockers for the safe custody of valuable assets of their customers such as gold, silver, legal documents etc.

(ii) Banks give reference for their customers.

(iii) Banks collect necessary and useful statistics relating to trade and industry.

(iv) For facilitating foreign trade, banks undertake to sell and purchase foreign exchange.

(v) Banks advise their clients relating to investment decisions as specialist

(vi) Bank does the under-writing of shares and debentures also.

(vii) Banks issue letters of credit.

(viii) During natural calamities, banks are highly useful in mobilizing funds and donations.

(ix) Banks provide loans for consumer durables like Car, Air-conditioner, and Fridge etc.

NAME: Uwode Joy Ogheneyonle

REG NO: 2107/241451

DEPARTMENT: Economics

EMAIL: yonlejoyuwode@gmail.com

Commercial banks play a significant role in our economy, as they act as a middle man between lenders and borrowers, as well as create credit, even though some commercial banks these days do misbehave and could be greedy, as they collect high charges on the service they provide to customers this making them enjoy excess profits. We also can’t leave out the important roles commercial banks play in our economy. These roles include issuance of money, settlement of payments, maturity transformation, money creation, acceptance of deposits, safekeeping of valuables, etc.

For an economy to function properly there must be existence of commercial banks as their important roles cannot be overemphasized and very useful for the economy to run efficiently.

Characteristics of insurable risks are those characteristics risks must posses before considered insurance and they include, Large number of similar exposure units, that is, risk to be insured should be common and not new. Define loss, that is loss take place at a known time in a known place and a known cause. Accidental loss, that is, the event that Constitutes the trigger of a claim should be outside the control of the beneficiary.

Large loss, that is, size of the loss must be meaningful from the perspective of the insured.

Affordable premium, that is if the likelihood of an invent is so high or the cost of an event is large then the resulting premium must be large relative to the amount of protection offered.

Calculable loss, Limited risk of catastrophically large loss, that is insurance losses are ideally independent and non catastrophic, all losses do not happen at once and individual losses do not happen to bankrupt the insurer.

In my own opinion, accidental loss is considered as the most important.

1. I believe banks are very relevant because they play important roles in the economy which includes

-Capital formation

-Channelizing the funds to productive Investment

-Fuller utilization of resources

-Encouraging right type of Industries

-Creation of Credit

-Finance to Government

-Private equity financing

-Purchase and Sale of securities

2. Seven characteristics of Insurable risks includes

-The loss should not be catastrophic.

-The chance of loss must be calculable.

-The premium must be economically feasible.

-There must be a large number of exposure units.

-The loss must be accidental and unintentional.

-The loss must be determinable and measurable.

-Fortuitous loss

I consider the loss should accidentally and unintentional to be the most important

And the loss must determinable and measurable as the least important

Name: ALI CHUKWUEMEKA JAPHET

Reg. No: 2017/242427

Dept: Economics (Major)

As we know the main objectives of a commercial bank are to earn profit by the process of accepting of deposits and advancing loans through different methods.

Although these functions are the basic function of commercial banks, but there are a lot more functions that enhance the importance of banks today and thus contribute so much to the development of the economy.

1. Provisions of agency and general utility services to his customers

2. Making new investments in different organizations and increasing the productive capacity of the country

3. Promote capital formation in the country by mobilizing and collection of savings for the purpose of investments

4. Development of industries in the country according to the requirements of the economy

5. Development in agricultural production is made possible by providing different kinds of loans

6. Commercial banks help in reducing reliance on foreign assistance by their efforts in the mobilization of domestic savings

7. These banks help in the implementation of an effective monetary policy according to the objective to the central bank.

8. Commercial banks also help in the creation and distribution of money through the sales and purchase of securities.

9. Commercial banks are the custodian and distributor of liquid capital of the country, which is the lifeblood of all commercial and economic activities of a country.

10. Commercial Banks provide short-term and medium- term loans in the industry. In Nigeria, they undertake financing of small scale industries and also provide hire-purchase finance.They not only provide finance for industry but also help in developing the capital market which is underdeveloped in such countries.

With these few points of mine, I totally agree that commercial banks play important roles in the economy.

B.

Insurance is a device that gives protection against risk. But not all both individual and commercial risks can be insured and given protection.

There are 7 Elements of insurable Risks:

1.Large numbers of exposure units.

2. Define and measurable loss.

3. Determinable probability distribution.

4. Calculable chance of loss.

5. Fortuitous loss.

6. Non-catastrophic loss.

7. Premium should be economically feasible.

For me, the law I appreciate most is the second one; the loss should be both determinable and measurable.

This means the loss should be definite as to cause, time, place, and amount. Life insurance is most cases meets this requirement easily. The cause and time of death can be readily determined in most cases, and if the person is insured, the face amount of the life insurance policy is the amount paid.

Thank you Mr. President!

Onaku Joseph Chibuzo

2016/234580

Economics

The functions of the commercial banks are certainly evident that we cannot ignore the fact that they are actually a composition in the entire financial system. Their functions are as follows though not all would be explained here;

1. Approval of deposits and valuables from customers: This very purpose is the topmost and apart from that, is actually what involves the customers’ deposits more. The commercial banks actually help save or rather accept deposits in form of money and other valuables mostly for safekeeping or in order to exhaust all at once. We would have that in the course of keeping this money in the banks, the banks tend to extort if I’m permitted to use that word the customers by charging different kind of charges like SMS alert fee every month, ATM maintenance fee every month as well. These and others have actually made people that are customers of various banks to complain and in fact doubt the functions of the commercial banks as to whether or not it is helping the customers or even trying to like extort then unnecessarily.

2. Requirement of Credit facilities: This implies that commercial banks help to create money in form of loans and overdrafts. But this also has caused issue as the commercial banks now charge unreasonable prices as interests on these loans and this forces customers to just maybe stop subscribing to loans from the commercial banks.

3. Provision of various payment platforms: The commercial banks have helped in this area as a customer can now order something online and even pay for it without having to come in contact with money or having to go to the ATM first to get cash. The customer could just transfer the money thereby making the while process a lot faster but the commercial banks have seen this as another portal though which the customers can keep their money with them and they can be able to take from it. A customer would want to make a transfer from a bank account to another bank account of which both accounts are under the same account but that bank would still charge for transfer which is quite unreasonable as why then did I transfer when I could just have gone to the counter to make the transfer through use of the deposit slip.

4. Mortgages to home buyers: The commercial banks provide loans for housing but some do so at a very high interest rate or giving a high demand for collaterals.

5. Provision of interest rate to savers: Those who practically save their money deposits in banks tend to get some interest though others do not have the opportunity to this as not all banks do it. Though the interest rate is small but at least the commercial banks are trying on this one.

A. Clearly there are seven listed risks that can be insured and these risks have to possess some characteristics before they can be referred to as being insurable. These fractures include:

1. Large number is similar exposure units: This basically means that the supposed risk to be insured should have happened more than once that is, the risk should not be the first of its kind as this alone would even discourage the insurance policy company to even want to insure that risk.

2. Definite Loss: The supposed risk must he caused or influenced by something relevant or important as anything contrary to this would make the insurance company not to even identify such individual.

3. Accidental Risk: The risk should not be premeditated that is it should be accidental in order for the insured to be indemnified.

4. Big Loss: This implies that the premium that’s been paid should be large or much to accommodate the weight of the loss.

5. Accessible Premium: The insurance company should charge premiums that is cheap and atoe to encourage more individuals to insure their properties or toner things insurable.

6. Calculable Loss: ever that is being insured should be able to be converted to costs whether it be a car or house, such should be able to be calculated and be given a premium with which to pay every month or thereabout as the case may be.

7. Limited risk of destructive large Loss: This means that the entire risks that have been insured by the insurance company cannot happen at the same time as this could make the insured company liquidate and therefore such risk must not be such that if several persons take It.

Insurance companies normally only indemnify against ordinary risk, otherwise known as event risks. A pure risk includes any uncertain situation where the opportunity for loss is present and the opportunity for financial gain is absent.

Speculative risks are those that might produce a profit or loss, namely business ventures or gambling transactions. Speculative risks lack the core elements of instability rarely lost never insured.

Examples of pure risks include natural events, such as fires or floods, or other accidents, such as an automobile crash or an athlete seriously injuring his or her knee. Most pure risks can be divided into three categories: personal risks that affect the income-earning power of the insured person, property risks, and liability risks that cover losses resulting from social interactions. Not all pure risks are covered by private insurers.

Name: oroke charity Nnedimma

Reg no: 2017/243816

Depart: Economics

Role of commercial Banks

1. Mobilising Saving for Capital Formation:

The commercial banks help in mobilising savings through network of branch banking. They also help in mobilizating idle savings from the few rich, which they channel into productive investment which in turn lead to capital formation.

2. Financing Industry:

The commercial banks finance the industrial sector in a number of ways ,They provide short-term, medium-term and long-term loans to industry.

3. Financing Trade:

The commercial banks help in financing both internal and external trade. The banks provide loans to retailers and wholesalers to stock goods in which they deal. They also help in the movement of goods from one place to another by providing all types of facilities such as discounting and accepting bills of exchange, providing overdraft facilities, issuing drafts, etc. Moreover, they finance both exports and imports of developing countries by providing foreign exchange facilities to importers and exporters of goods.

4. Financing Agriculture:

The commercial banks help the large agricultural sector in developing countries in a number of ways. They provide loans to traders in agricultural commodities. They open a network of branches in rural areas to provide agricultural credit. They provide finance directly to agriculturists for the marketing of their produce, for the modernisation and mechanisation of their farms, for providing irrigation facilities, for developing land

5. Financing Consumer Activities:

People in underdeveloped countries being poor and having low incomes do not possess sufficient financial resources to buy durable consumer goods. The commercial banks advance loans to consumers for the purchase of such items as houses, scooters, fans, refrigerators, etc. In this way, they also help in raising the standard of living of the people in developing countries by providing loans for consumptive activities

6. Financing Employment Generating Activities:

The commercial banks finance employment generating activities in developing countries. They provide loans for the education of young person’s studying in engineering, medical and other vocational institutes of higher learning. They advance loans to young entrepreneurs, medical and engineering graduates, and other technically trained persons in establishing their own business.

7. Help in Monetary Policy:

The commercial banks help the economic development of a country by faithfully following the monetary policy of the central bank. In fact, the central bank depends upon the commercial banks for the success of its policy of monetary management in keeping with requirements of a developing economy.

7 characteristics of insurable risk

1.larg no of similar exposure units:since Insurance operate by pooling resources together , it then mean that a good number of people should be expose to similar risk , such that the insurance company will be able to realize resources which it operate with.

2.Definit loss : the loss has to be definite in nature in the sense that, the cause , the place it occurred and the time it occurred must be known

3. Accidental loss: This imply that event that constitutes or lead to the loss to occur must be beyond the control of the beneficiary.

4. Large loss : the loss should be to a reasonable one , and not when you insure your car and had a little scratch you start going for indemnity.

5. Affordable premium: if the likelihood of the occurrence of an event is high, the cost of the event so high that the resulting premium is so large relative to the amount of the protection offered,then it is not likely that the insurance card will be purchased, even if on offer .

6. Caculable loss : insurable risk must be caculable in the sense that , the probability of loss and attndant cost must be calculable.

7. Limited risk of catastrophically larg losses : this implys that the insurable should not such that in capable of happening once , or such that is capable of bankrupting the the insurance company.

NAME: OKEKE JUDE CHIMOBI

REG NO: 2017/249556

DEPARTMENT: ECONOMICS

EMAIL: chimobiokeke@gmail.com

Banks are very relevant in the economy and their roles are very significant in the economy. Some important roles of banks include:

1. Safety of deposits

Banks are seen as a secure place to deposit money. It would be impractical and risky to keep all your savings as cash under your bed. In medieval times, people would often pay early banks (e.g. Knights Templar) to keep their money and assets safe. It also saves people worrying about money.

2. Interest on deposits

Commercial banks pay interest on deposits. For current accounts, this may be very low, but for saving accounts, the interest rate can be significant. In a period of inflation, interest rates on deposits are very important for maintaining the real value of your savings.

3. Loans

A bank can become more profitable by using a percentage of its deposits to lend to other customers. If a bank pays 2% on bank deposits but lends money to firms and consumers at 6%, then it can make a bigger profit on its deposits. A bank just needs to keep sufficient liquidity to meet the demands of customers to withdraw money.

Different types of bank lending:

Different interest rates on different types of loans.

Bank lending varies from unsecured personal loans to secured mortgage lending. Unsecured lending tends to be at a higher interest rate because of the risk factor. Secured mortgage lending is at a lower rate, but can be over 30 years or more.

Personal loan – In this case, the bank may make a loan to be paid back over a few years. This loan may be unsecured against any assets like a house. Personal loans could be for a big purchase like a car or specifically to help fund a career or educational improvement.

Business loan – A loan for a firm to invest and expand their business.

Mortgage – This is a special type of loan, where the bank advances a loan to purchase a house. Usually, the customer will need to pay a deposit on the house, e.g. 10% of the loan. The bank legally owns the house until the borrowers have finished paying back the mortgage payments over a period of 20-40 years. Interest rates on mortgages tend to be relatively low because the loan is secured against the value of the house. However, on a 30-year mortgages, home-buyers will typically pay more interest than the total cost of the house.

Overdraft – A bank can agree on an overdraft with customers. This allows them to borrow money in the short term quickly and conveniently. However, the amount allowed tends to be quite small.

4. Capital Formation

Banks play an important role in capital formation, which is essential for the economic development of a country. They mobilize the small savings of the people scattered over a wide area through their network of branches all over the country and make it available for productive purposes.

5. Creation of Credit

Banks create credit for the purpose of providing more funds for development projects. Credit creation leads to increased production, employment, sales and prices and thereby they bring about faster economic development.

6. Encouraging Right Type of Industries

Many banks help in the development of the right type of industries by extending loan to right type of persons. In this way, they help not only for industrialization of the country but also for the economic development of the country. They grant loans and advances to manufacturers whose products are in great demand. The manufacturers in turn increase their products by introducing new methods of production and assist in raising the national income of the country.

7. Employment Generation

After the nationalization of big banks, banking industry has grown to a great extent. Bank’s branches are opened frequently, which leads to the creation of new employment opportunities.

8. Banks Promote Entrepreneurship

In recent days, banks have assumed the role of developing entrepreneurship particularly in developing countries by inducing new entrepreneurs to take up the well-formulated projects and provision of counseling services like technical and managerial guidance.

INSURABLE RISKS

Characteristics of Insurable Risks:

Risks must have the following features before it can be insurable.

a. Large number of similar exposure units: The prime necessity for a risk to be insurable is that there must be a sufficiently large number of homogeneous exposures to combine reasonably predictable losses. An insurable risk should have more than one if its kind, that is, it is not supposed to be only one of its kind.

b. Definite loss: The loss should be determinable. This means the loss should be definite as to cause, time, place, and amount. Life insurance is most cases meets this requirement easily. There has to be a named or particular cause of the loss.

c. Accidental loss: An insurable risk must have the prospect of accidental loss, meaning that the loss must be the result of an unintended action and must be unexpected in its exact timing and impact.

The insurance industry normally refers to this as “due to chance.” Insurers only pay out claims for loss events brought about through accidental means. It protects against intentional acts of loss, such as a landlord burning down his or her own building.

d. Large loss: This means that the premium must be large enough to cover the large loss.

e. Affordable premium: The insured must be able to pay the premium.

f. Calculable loss: The insurer must be able to calculate both the average frequency and the average severity of future losses with some accuracy. This requirement is necessary so that a proper premium can be charged that is sufficient to pay all claims and expenses and yield a profit during the policy period.

g. Limited risk of catastrophically large loss: The losses should be non-catastrophic. Not all the units in a homogeneous group will be subject to an adverse event. This means that a large proportion of exposure units should not incur losses at the same time. As we stated earlier, pooling is the essence of insurance. If most or all of the exposure units in a certain class simultaneously incur a loss, then the pooling technique breaks down and becomes unworkable. Losses cannot happen all at once for all insured persons. That is, insurable losses are ideally independent and non-catastrophic.

All the characteristics are equally important.

NAME: UMELO CHIDERA NICOLE

REGISTERATION NUMBER: 2017/249589

EMAIL: nicoleumelo@gmail.com

1. The global financial system is one that raises in a person feelings mixed with doubt and confusion. Needed to set the pace for economic development, one often wonders if the financial system should be considered a pace setter or perhaps an entity for limitation. So many limitation exists in the context of the financial system, not in the least are the anti- developmental practices of financial institutions in different countries of the world, one often begins to wonder if the financial system is so important that it cannot be done without, and if, indeed it can be done without, what better alternatives exist for the use of the masses? Although many may argue otherwise, the fact remains that banks and other financial institutions play pertinent and delicate roles for economic sustenance. The problem therein lies in the “bad” practices of these banks. For instance, why do banks continue to charge exorbitant fees simply for banking services offered, or why do banks continue, in spite of their heavy fees, to provide services that are not up to par? The problems faced by different citizens in different parts of the global economy especially those related to the banking and financial sectors, have thus created an increased feeling of dread and dismay, so much so that the mechanical female voice at the end of every transaction at the ATM saying “thank you for banking with us” becomes suspect. Are banks and financial institutions ripping off the masses for organizational gains?

From personal perspective, this question is highly subjective. Hence from personal perspective, I believe that although the charges from banks are actually useful and important for the smooth flow of all economic activities, a check should be placed on the extent of these charges.

In the global economy, one major problem persists; the problem of financial inclusion, or financial apathy if one is so inclined. A person will be hard-pressed to sing the praises of any bank or financial institution in face of such glaring circumstance. A person will in fact, totally give up on the concept of banking as a whole if such conditions persist. Hence my recommendation for a revised system of affairs. The central bank should work together with commercial banks and other financial institutions to procure a reasonable level of lending rate and bank rates. This is done to encourage financial inclusion as well as commercial lending and investment in the country.

2. THE SEVEN CHARACTERISTICS OF INSURABLE RISK

One day, a man went to an insurance company to purchase an insurance policy. He had with him, his 30-year-old Volkswagen whose breaks was faulty, and was gunning to obtain an automobile insurance policy. At his arrival, the insurance agent discussed with him the seven features of an insurable risk. These features are:

A. Large number of similar exposure units: this means that there must be a substantial amount of people exposed to the same risk.

B. Definite loss: in the event of the insured risk, the loss should take place at a known day, time and for a known cause

C. Accidental loss: this implies that the loss or the occurrence of the loss should be outside the control of the insured

D. Large loss: the loss or the occurrence of the loss should be meaningful to the insured.

E. Affordable premium: this has to do with the likelihood of the event occurring. A high risk results in a higher premium

F. Calculable loss: The loss must be calculable

G. Limited risk of catastrophically large losses: the event of a loss should not lead to a chain of other losses also occurring.

Hence, since his car could not meet most of these features, this man was sent back home, although he did come back the next day to assure his life. Personally, I believe the most important feature is the feature of accidental loss. This is because it helps to prevent any foul play.

Thank you.

Okororie Emmanuel Kelechi

2017/242947

Economics

ROLE OF COMMERCIAL BANK IN THE ECONOMY.

1. Collections of Savings and Advancing Loans

Acceptance of deposit and advancing the loans is the basic function of commercial banks. On this function, all other functions depend accordingly. Bank operates different types of accounts for its customers.

2. Money Transfer

Banks have facilitated the making of payments from one place or persons to another by means of cheques, bill of exchange and drafts, instead of cash. Payment through cheques, the draft is more safe and convenient, especially in case of huge payments, this facility is a great help for traders and businessmen. It really enhances the importance of banks for the business community.

3. Encourages Savings

Banks perform an invaluable service by encouraging savings among the people. They induce them to save for profitable investment for themselves and for the national interest. These savings help in capital formation.

4. Transfer Savings into Investment

Bank transfer the savings collected from the people into investment and thus increase the amount of effective capital, which helps the process of economic growth.

5. Overdraft Facilities

The banks allow the overdraft facilities to their trusted customers and thus help them in overcoming temporary financial difficulties.

6. Discounting Bill of Exchange

The importance of banks can be seen through the facility of discounting the bill of exchange. Banks discount their bill of exchange of consumers and help them in financial difficulties. By discounting a bill of exchange, they able to get the desired amount for the investment they want.

CHARACTERISTICS OF INSURABLE RISKS:

There must be a large number of exposure units.

The loss must be accidental and unintentional.

The loss must be determinable and measurable.

The loss should not be catastrophic.

The chance of loss must be calculable.

The premium must be economically feasible.

NAME: IJARA PETER ELOCHUKWU

DEPARTMENT: ECONOMICS

REG NO: 2017/249513

EMAIL: petochris86@yahoo.com

Eco 324

(1)

Financing Industrial Sector: Banks provide short-term, medium- term and long term loans in the industrial sector. In India, they undertake financing of small scale industries and also provide hire-purchase finance. These banks not only provide finance for industry.

Financing Industrial Sector: Banks provide short-term, medium- term and long term loans in the industrial sector. In India, they undertake financing of small scale industries and also provide hire-purchase finance. These banks not only provide finance for industry.

Help in developing the capital market which is underdeveloped in such countries.

Help in developing the capital market which is underdeveloped in such countries. They Help in Mobilising Saving for Capital Formation: The commercial banks help in mobilising savings through network of branch banking. People in LDCs countries have low incomes but the banks induce them to save by introducing varieties of packages to suit the needs of individual depositors. They also mobilise idle savings of the few rich. By mobilising savings, the savings are now used to provide loans for investment. However, in order for banks to run their daily activities effectively they charge their customers bank fees results for the services rendered to customers.

They Help in Mobilising Saving for Capital Formation: The commercial banks help in mobilising savings through network of branch banking. People in LDCs countries have low incomes but the banks induce them to save by introducing varieties of packages to suit the needs of individual depositors. They also mobilise idle savings of the few rich. By mobilising savings, the savings are now used to provide loans for investment. However, in order for banks to run their daily activities effectively they charge their customers bank fees results for the services rendered to customers.

Banks as financial institution render lots of services to customers and the public. Some include :

,

Example of bank charges paid by customers include :Bank account maintenance fee, ATM withdrawal bank fees, Fees charged for overdrafts and insufficient funds, wire transfer fees both in and out of an account.

(2)

The characteristics of insurable risks are the features that sellers and buyers of insurance policies should look for when selling or buying insurance policies. All 7 characteristics are effective and equally important to have a desired insurance policy. And so that no party feels cheated.

The characteristics include large number of similar exposure unit, definite loss, loss must not be intentional, the loss must be meaningful from the view of the insured, the premium must be affordable by the insured, calculable loss, limited risk of catastrophically large losses.

NAME: IJE VORDA GOODNESS

DEPARTMENT: ECONOMICS

REG NO: 2017/249514

EMAIL: vordagoodness78@gmail.com

Course: Eco 324

ANSWER ONE

Banks provide loans to firms for investment purposes. This funds are then used to expand and upgrade the firm’s so as to improve their productivity so invariably banks improve the productive capacity of the economy. Interest rate are also charged by the banks on the loans they give the public which help to generate money. However deposit with the banks can be used to generate as 10times what was deposited.

Banks provide loans to firms for investment purposes. This funds are then used to expand and upgrade the firm’s so as to improve their productivity so invariably banks improve the productive capacity of the economy. Interest rate are also charged by the banks on the loans they give the public which help to generate money. However deposit with the banks can be used to generate as 10times what was deposited.

Bank act as financial agents and adviser to their customers. They also aid payment band transactions.

Bank act as financial agents and adviser to their customers. They also aid payment band transactions.

The banking system help in the supply of money to the economy.

The banking system help in the supply of money to the economy. Banks play a major role in internal and international trade. A large part of trade is done on credit. Banks provide references and guarantees, on behalf of customer,on behalf of customers, on the basis of who can supply goods on credit.

Banks play a major role in internal and international trade. A large part of trade is done on credit. Banks provide references and guarantees, on behalf of customer,on behalf of customers, on the basis of who can supply goods on credit.

Bank account maintenance fees, and if your account is for earning interest monthly maintenance fees will effectively cancel out potential earnings on the account.

Bank account maintenance fees, and if your account is for earning interest monthly maintenance fees will effectively cancel out potential earnings on the account.

ATM withdrawal bank fees.

ATM withdrawal bank fees.

Fees charged for overdrafts and insufficient funds.

Fees charged for overdrafts and insufficient funds. Charging fee to wire transfer both in and out of an account.

Charging fee to wire transfer both in and out of an account.

The importance of the banks in the economy cannot be over emphasized. Banks control the supply of money in circulation in an economy.

️

However, in order for banks to run their day to day activities effectively they charge their customers a token which results from the services rendered to customers.

Example of bank charges paid by customers include

️

So banks are very important in the society and charge bank fees to facilitate it’s smooth running.

ANSWER TWO

The characteristics of insurable risks are the features that insurance firms and buyers of insurance policies should look for when selling or buying insurance policies. All of the 7 characteristics are effective and equally important to have a desired insurance policy.

They include large number of similar exposure unit, definite loss, loss must not be intentional, the loss must be meaningful from the view of the insured, the premium must be affordable by the insured, calculable loss, limited risk of catastrophically large losses. However all the 7 characteristics are effective and equally important to have a desired insurance policy.

Name: ONAH GEORGE CHIEDOZIE.

REG. NO: 2017/241453.

DEPARTMENT: ECONOMICS.

Commercial bank is a financial institution that accepts deposit from the members of the public. It performs some roles which include thus:

_Financing Industrial Sector:

Commercial Banks provide short-term and medium- term loans in the industry. In India, they undertake financing of small scale industries and also provide hire-purchase finance. These banks not only provide finance for industry but also help in developing the capital market which is underdeveloped in such countries.

_Mobilising Saving for Capital Formation:

The commercial banks help in mobilising savings through network of branch banking. People in developing countries have low incomes but the banks induce them to save by introducing variety of deposit schemes to suit the needs of individual depositors. They also mobilise idle savings of the few rich. By mobilising savings, the banks channelise them into productive investments. Thus they help in the capital formation of a developing country.

_Financing Employment Generating Activities:

The commercial banks finance employment generating activities in developing countries. They provide loans for the education of young person’s studying in engineering, medical and other vocational institutes of higher learning. They advance loans to young entrepreneurs, medical and engineering graduates, and other technically trained persons in establishing their own business. Such loan facilities are being provided by a number of commercial banks in India. Thus the banks not only help inhuman capital formation but also in increasing entrepreneurial activities in developing countries.

The 7 characteristics of insurable insurable risk include:

1. Large Numbers of Exposure Units:

Therefore the prime necessity for a risk to be insurable is that there must be a sufficiently large number of homogeneous exposures to combine reasonably predictable losses.

Lost data can be compiled over time, and losses for the group as a whole can be predicted with some accuracy. The loss costs can then be spread over all insured’s in the underwriting class.

2. Determinable Probability Distribution

The probability distribution of happening of an adverse event if determinable. This condition is necessary to establish a free premium according to the theory of equivalence.

If there is not determinable distribution, there is no question of issuing a cover by an insurance company.

3. Define and Measurable Loss:

A third requirement is that the loss should be both determinable and measurable. This means the loss should be definite as to cause, time, place, and amount. Life insurance is most cases meets this requirement easily.

4. Calculable Chance of Loss:

A fourth requirement is that the chance of loss should be calculable. The insurer must be able to calculate both the average frequency and the average severity of future losses with some accuracy.

5.Fortuitous Loss:

The adverse event may or may not occur in the future and once the insurance company has no control. Naturally, if the event is non-random or the loss has occurred in the past, there is no question of insurance.

6.The losses should be non-catastrophic:

Not all the units in a homogeneous group will be subject to an adverse event. This means that a large proportion of exposure units should not incur losses at the same time.

7. Premium Should be Economically Feasible:

It is the final requirement that the premium should be economically feasible. The insured must be able to pay the premium.

Also, for the insurance to be an attractive purchase, the premiums paid must be substantially less than the face value, or amount, of the policy.

Name: Ani Gabriel Ogbonna

Reg. Number: 2017/249483

Email : anigabriel05@gmail.com

THE ROLE OF COMMERCIAL BANKS IN THE ECONOMY

Commercial Banks have always played an important position in the country’s economy. They play a decisive role in the development of the industry and trade. They are acting not only as the custodian of the wealth of the country but also as resources of the country, which are necessary for the economic development of a nation.

The role of commercial banks includes the following;

1. Capital Formation

Banks play an important role in capital formation, which is essential for the economic development of a country. They mobilize the small savings of the people scattered over a wide area through their network of branches all over the country and make it available for productive purposes. Now-a-days, banks offer very attractive schemes to attract the people to save their money with them and bring the savings mobilized to the organized money market. If the banks do not perform this function, savings either remains idle or used in creating assets, which are low in scale of plan priorities.

2. Creation of Credit

Banks create credit for the purpose of providing more funds for development projects. Credit creation leads to increased production, employment, sales and prices and thereby they cause faster economic development.

3. Channelizing the Funds to Productive Investment

Banks invest the savings mobilized by them for productive purposes. Capital formation is not the only function of commercial banks. Pooled savings should be distributed to various sectors of the economy with a view to increase the productivity of the nation. Then only it can be said to have performed an important role in the economic development of the nation. Commercial Banks aid the economic development of the nation through the capital formed by them. In India, loan lending operation of commercial banks subject to the control of the RBI. So our banks cannot lend loan, as they like.

4. Fuller Utilization of Resources

Savings pooled by banks are utilized to a greater extent for development purposes of various regions in the country. It ensures fuller utilization of resources.

5. Encouraging Right Type of Industries

The banks help in the development of the right type of industries by extending loan to right type of persons. In this way, they help not only for industrialization of the country but also for the economic development of the country. They grant loans and advances to manufacturers whose products are in great demand. The manufacturers in turn increase their products by introducing new methods of production and assist in raising the national income of the country.

6. Finance to Government

Government is acting as the promoter of industries in underdeveloped countries for which finance is needed for it. Banks provide long-term credit to Government by investing their funds in Government securities and short-term finance by purchasing Treasury Bills.

CHARACTERISTICS OF INSURABLE RISK.

Insurance is a device that gives protection against risk. But not all both individual and commercial risks can be insured and given protection. The 7 element of insurable risk includes;

1. Large Numbers of Exposure Units