- The Legal principles of insurance are very fundamental for the smooth operations of insurance business. Cleary discuss and analyse the seven principles of insurance and the insurance business model using relevant examples.

- In an environment where there is so much antagonism towards insurance business, what would be your advice to an employee who works in an insurance company, and has been given a specific period of time to get a group of clients who will insure their assets/properties or even buy life assurance policies? How can such a staff meet the target?

- Given the scenario above, assuming you are the owner of the insurance firm, what will you do to increase the patronage of clients towards your insurance business?

Question 1

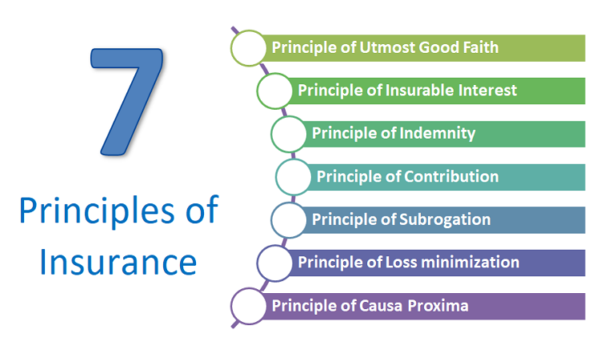

PRINCIPLE OF INSURABLE INTEREST

The principle of insurable interest states that the person getting insured must have insurable interest in the object of insurance.A person has an insurable interest when the physical existence of the insured object gives him some gain but its non-existence will give him a loss. In simple words, the insured person must suffer some financial loss by the damage of the insured object.

PRINCIPLE OF UTMOST GOOD FAITH

Principle of Uberrimae fidei (a Latin phrase), or in simple english words, the Principle of Utmost Good Faith, is a very basic and first primary principle of insurance. According to this principle, the insurance contract must be signed by both parties (i.e insurer and insured) in an absolute good faith or belief or trust.

PRINCIPLE OF UTMOST GOOD FAITH

The person getting insured must willingly disclose and surrender to the insurer his complete true information regarding the subject matter of insurance. The insurer’s liability gets void (i.e legally revoked or cancelled) if any facts, about the subject matter of insurance are either omitted, hidden, falsified or presented in a wrong manner by the insured.This principle applies to all types of insurance contracts.

PRINCIPLE OF INDEMNITY

Indemnity means security, protection and compensation given against damage, loss or injury. According to the principle of indemnity, an insurance contract is signed only for getting protection against unpredicted financial losses arising due to future uncertainties. Insurance contract is not made for making profit else its sole purpose is to give compensation in case of any damage or loss.

PRINCIPLE OF CONTRIBUTION

Principle of Contribution is a corollary of the principle of indemnity. It applies to all contracts of indemnity, if the insured has taken out more than one policy on the same subject matter.According to this principle, the insured can claim the compensation only to the extent of actual loss either from all insurers or from any one insurer. If one insurer pays full compensation then that insurer can claim proportionate claim from the other insurers.

For example :- Mr. John insures his property worth Rs.100,000 with two insurers “AIG Ltd.” for Rs. 90,000 and “MetLife Ltd.” for Rs. 60,000.John’s actual property destroyed is worth Rs. 60,000, then Mr. John can claim the full loss of Rs. 60,000 either from AIG Ltd. or MetLife Ltd., or he can claim Rs. 36,000 from AIG Ltd. and Rs. 24,000 from Metlife Ltd.

PRINCIPLE OF SUBROGATION

Subrogation means substituting one creditor for another. Principle of Subrogation is an extension and another corollary of the principle of indemnity. It also applies to all contracts of indemnity. According to the principle of subrogation, when the insured is compensated for the losses due to damage to his insured property, then the ownership right of such property shifts to the insurer. This principle is applicable only when the damaged property has any value after the event causing the damage. The insurer can benefit out of subrogation rights only to the extent of the amount he has paid to the insured as compensation.

For example :- Mr. John insures his house for Rs.1 million. The house is totally destroyed by the negligence of his neighbour Mr.Tom. The insurance company shall settle the claim of Mr. John for Rs. 1 million. At the same time, it can file a law suit against Mr.Tom for Rs. 1.2 million, the market value of the house. If insurance company wins the case and collects Rs. 1.2 million from Mr. Tom, then the insurance company will retain Rs. 1 million (which it has already paid to Mr. John) plus other expenses such as court fees. The balance amount, if any will be given to Mr. John, the insured.

PRINCIPLE OF LOSS MINIMIZATION

According to the Principle of Loss Minimization, insured must always try his level best to minimize the loss of his insured property, in case of uncertain events like a fire outbreak or blast, etc. The insured must take all possible measures and necessary steps to control and reduce the losses in such a scenario. The insured must not neglect and behave irresponsibly during such events just because the property is insured. Hence it is a responsibility of the insured to protect his insured property and avoid further losses.

PRINCIPLE OF CAUSA PROXIMA (NEAREST CAUSE)

means when a loss is caused by more than one causes, the proximate or the nearest or the closest cause should be taken into consideration to decide the liability of the insurer. The principle states that to find out whether the insurer is liable for the loss or not, the proximate (closest) and not the remote (farest) must be looked into.

For example :- A cargo ship’s base was punctured due to rats and so sea water entered and cargo was damaged.Here there are two causes for the damage of the cargo ship – (i) The cargo ship getting punctured beacuse of rats, and (ii) The sea water entering ship through puncture. The risk of sea water is insured but the first cause is not. The nearest cause of damage is sea water which is insured and therefore the insurer must pay the compensation. However, in case of life insurance, the principle of Causa Proxima does not apply. Whatever may be the reason of death (whether a natural death or an unnatural death) the insurer is liable to pay the amount of insurance.

Question 2

As an insurance agent, I would convince the prospective client to get and insurance package by telling the person about the benefits of the insurance package and also the chances of experiencing an incident.

Question 3

As the owner of an insurance firm, I would make sure I explain properly the terms of the insurance contract to the clients and also indemnify them when they suffer a loss that the insurance contract covers

ENEH KENECHUKWU

2017/249496

ECONOMICS

————————————————————————————–

The Legal principles of insurance are very fundamental for the smooth operations of insurance business. Cleary discuss and analyse the seven principles of insurance and the insurance business model using relevant examples

1. Nature of contract:Nature of contract is a fundamental principle of insurance contract. An insurance contract comes into existence when one party makes an offer or proposal of a contract and the other party accepts the proposal.

A contract should be simple to be a valid contract. The person entering into a contract should enter with his free consent.

2. Principal of utmost good faith:

Under this insurance contract both the parties should have faith over each other. As a client it is the duty of the insured to disclose all the facts to the insurance company. Any fraud or misrepresentation of facts can result into cancellation of the contract.

3. Principle of Insurable interest: Under this principle of insurance, the insured must have interest in the subject matter of the insurance. Absence of insurance makes the contract null and void. If there is no insurable interest, an insurance company will not issue a policy.

An insurable interest must exist at the time of the purchase of the insurance. For example, a creditor has an insurable interest in the life of a debtor, A person is considered to have an unlimited interest in the life of their spouse etc.

4. Principle of indemnity:

Indemnity means security or compensation against loss or damage. The principle of indemnity is such principle of insurance stating that an insured may not be compensated by the insurance company in an amount exceeding the insured’s economic loss.

In type of insurance the insured would be compensation with the amount equivalent to the actual loss and not the amount exceeding the loss.

This is a regulatory principal. This principle is observed more strictly in property insurance than in life insurance.

The purpose of this principle is to set back the insured to the same financial position that existed before the loss or damage occurred.

5. Principal of subrogation:

The principle of subrogation enables the insured to claim the amount from the third party responsible for the loss. It allows the insurer to pursue legal methods to recover the amount of loss, For example, if you get injured in a road accident, due to reckless driving of a third party, the insurance company will compensate your loss and will also sue the third party to recover the money paid as claim.

6. Double insurance:

Double insurance denotes insurance of same subject matter with two different companies or with the same company under two different policies. Insurance is possible in case of indemnity contract like fire, marine and property insurance.

Double insurance policy is adopted where the financial position of the insurer is doubtful. The insured cannot recover more than the actual loss and cannot claim the whole amount from both the insurers.

7. Principle of proximate cause:

Proximate cause literally means the ‘nearest cause’ or ‘direct cause’. This principle is applicable when the loss is the result of two or more causes. The proximate cause means; the most dominant and most effective cause of loss is considered. This principle is applicable when there are series of causes of damage or loss.

In an environment where there is so much antagonism towards insurance business, what would be your advice to an employee who works in an insurance company, and has been given a specific period of time to get a group of clients who will insure their assets/properties or even buy life assurance policies? How can such a staff meet the target?

Well using nigeria as a case study its obvious people buying insurace premium are realtively lower compared to the developed nations as people even struggle to live above a dollar, the best markteing strategy is targetted ads towars the rich class, make them undersatsn the impotance of having insurance and its long term benefit.

the ads could be radio programmes Tv shows etc

Given the scenario above, assuming you are the owner of the insurance firm, what will you do to increase the patronage of clients towards your insurance business?

i wold inlove more on targetted ads as well as enlightening people on what insurace means the advantages,risk invloved in living withpout insurance and how to go about it, most people are void of knowledge educating them would also act as a stimulating towrds getting insured.

Name: Ezeamaku Chukwuemeka Victor

Reg no: 2017/243370

Dept: Economics

Question 1

The seven principles of insurance;

a. Principle of Indemnity: This principle states that the insurance company which is also called the insurer should restore the insured back to the position he or she was before the loss occurred given the insureds premium. In the event of a loss the indemnity given to the insured should restore the insured to the position the insured was before suffering the loss

b. Principle of Insurable Interest: This is a principle that states that an insured may not collect more than its own financial interest in property that is damaged or destroyed.

C. Principle of Utmost Good Faith: This is a principle of full disclosure, that states that the insured should disclose every information about the asset being insured to the insurer, a breach of this principle can give grounds to a neglect in compensation.

d. Principle of Contribution: This principle states that insurance companies can come together to combine resources to indemnify a customer should in the case the companies have the same obligations to fulfill to the insured according to some stipulated methods.

e. Principle of Subrogation: This principle states that the insurance company has legal rights to pursue whatever concerns the insured on his behalf.

f. Principle of Proximate Cause: The cause of loss must be covered under the insuring agreement of the policy and the dominant cause must not be excluded.

g. Principle of Mitigation: This principle states that in the case of any loss that’s been insured, the insured should treat that property as if it weren’t insured at all.

Question 2

My advice to the employee who have to convert a certain number of clients is solely that of improved marketing technique, education of the need to do it and framing a good insurance plan, it’s all down to marketing strategies.

Question 3

A good name takes the Cake in this industry, as an insurer I will be committed to properly indemnifying my current customer base and aggressively advertise based solely on that performance.

Name:Eze Udoka Chidiebube

Reg no:2017/242428

Dept:Economics

1. Nature of contract:

Nature of contract is a fundamental principle of insurance contract. An insurance contract comes into existence when one party makes an offer or proposal of a contract and the other party accepts the proposal.A contract should be simple to be a valid contract. The person entering into a contract should enter with his free consent.

2. Principal of utmost good faith:Under this insurance contract both the parties should have faith over each other. As a client it is the duty of the insured to disclose all the facts to the insurance company. Any fraud or misrepresentation of facts can result into cancellation of the contract.

3. Principle of Insurable interest:Under this principle of insurance, the insured must have interest in the subject matter of the insurance. Absence of insurance makes the contract null and void. If there is no insurable interest, an insurance company will not issue a policy.An insurable interest must exist at the time of the purchase of the insurance. For example, a creditor has an insurable interest in the life of a debtor, A person is considered to have an unlimited interest in the life of their spouse etc.

4. Principle of indemnity:Indemnity means security or compensation against loss or damage. The principle of indemnity is such principle of insurance stating that an insured may not be compensated by the insurance company in an amount exceeding the insured’s economic loss.In type of insurance the insured would be compensation with the amount equivalent to the actual loss and not the amount exceeding the loss.This is a regulatory principal. This principle is observed more strictly in property insurance than in life insurance.The purpose of this principle is to set back the insured to the same financial position that existed before the loss or damage occurred.

5. Principal of subrogation:The principle of subrogation enables the insured to claim the amount from the third party responsible for the loss. It allows the insurer to pursue legal methods to recover the amount of loss, For example, if you get injured in a road accident, due to reckless driving of a third party, the insurance company will compensate your loss and will also sue the third party to recover the money paid as claim.

6. Double insurance:

Double insurance denotes insurance of same subject matter with two different companies or with the same company under two different policies. Insurance is possible in case of indemnity contract like fire, marine and property insurance.

Double insurance policy is adopted where the financial position of the insurer is doubtful. The insured cannot recover more than the actual loss and cannot claim the whole amount from both the insurers.

7. Principle of proximate cause:

Proximate cause literally means the ‘nearest cause’ or ‘direct cause’. This principle is applicable when the loss is the result of two or more causes. The proximate cause means; the most dominant and most effective cause of loss is considered.

B.How can an insurance worker meet up with the target?

1) Be a Connector

I’m sure you’ve heard this one before, but there’s more to helping people connect with each other than you may have considered.

2) Show Up to Events Early

I understand the temptation to show up fashionably late – it’s a lot easier to blend into a full room of people and its more likely you’ll see someone you already know.

3) Find More Networking Events.There are a lot more opportunities than just the local chamber of commerce.Think outside the box, ask around, and check out this list to get you thinking:

Chambers of Commerce

Business Networking Groups

Mastermind Groups7) Set Networking Goals

Like anything in business, proper goals will improve your results.

4)Make a measurable goal for networking like adding new LinkedIn Connections, giving away a certain number of business cards, or sending a certain number of follow-up emails to your contacts.

As an insurance owner,what wil you do to increase the patronage of clients towards insurance business?

1. Offer a free newsletter

Free is something that everyone can afford, from small businesses to global corporations. When you offer a free newsletter, you are informing your potential customers that you are willing to provide free information from the start.

2. Increase your customer base by asking for opinions

Before a web visitor leaves your website, request that they complete a short survey related to your business. People are happy to express themselves and often enjoy telling you about their online and offline experiences.

3. Keep up and maintain excellent customer support and service

A customer who contacts customer support about their first order is just as important as a customer who contacts customer service about their tenth order. Treat each customer with respect and take appropriate action.

4. Keep your website content fresh

Fresh and informative content is one of the main elements that pull in new visitors and potential customer.

5. Promote your business on social media networks

Facebook users have an average of 229 friends. When you create new content, launch a new product or run a new campaign, be sure you share this across the social media channels you are active in.

Reg no: 2017/249521

Dept: Economics

Introduction

Insurance is affected by legal agreements called contracts or policies. A contract cannot be complete in effect, but must be interpreted in light of the social environment of the society in which it is made. The legal principles of insurance that are generally applicable are discussed as follows.

4.1 Principle of Indemnity

The principle of indemnity is one of the most important legal principles in the field of insurance. The principle of indemnity states that the insured should not profit from a covered loss but should be restored to approximately the same financial position that existed prior to the loss. Most of the property insurance contracts are indemnity contracts. If a covered loss occurs, the insured should not collect more than the actual amount of the loss.

The principle of indemnity has two fundamental purposes: The first purpose is to prevent the insured from profiting from insurance. The insured should not profit if a loss occurs, but should be restored to approximately the same financial position that existed before the loss. For example, if Mr.X has insured his house for 100,000 birr and a loss amounted to 10,000 birr occurs, the principle of indemnity would be violated if 100,000 birr were paid to him; because he would be profiting out of insurance. The second purpose is to reduce moral hazard. If dishonest insured can profit from a loss, they may deliberately cause a loss with the intention of collecting the insurance. Thus, if the loss payment does not exceed the actual amount of the loss, the temptation to be dishonest is reduced.

Actual Cash Value Method:

In property insurance, the standard method of indemnifying the insured is based on the actual cash value of the damaged property at the time of loss. The Courts have used three major methods to determine actual cash value: Replacement cost less depreciation, Fair market value and Broad Evidence rule

Replacement cost less depreciation: Under this rule, actual cash value is defined as replacement cost less depreciation. This rule has been traditionally used to determine the actual cash value of property in property insurance. It takes into consideration both inflation and depreciation of property values over time. Replacement cost is current cost of restoring the damaged property with new materials of same kind and quality. Depreciation is a deduction for physical wear and tear, age and economic obsolescence. For example, machinery has been insured against fire. It burnt out of a fire. Assume that the machinery was bought 5 years ago and that machinery is 50% depreciated. The similar machinery would cost 10,000 birr. Under the actual cash value rule, the insured will collect only 5,000 birr for the loss of the machinery, because the replacement cost is 10,000 birr, but depreciation is 5,000 birr or 50%. If the insured were paid the full replacement value of 10,000 birr, the principle of indemnity would be violated, because the insured would be receiving the value of new brand machinery instead of one 5 years old. In short, 5,000 birr payment represents indemnification for the loss of 5 years old machinery.

Fair Market Value: Fair market value is the price a willing buyer would pay a willing seller in a free market. The fair market value of a building may be below its actual cash value based on replacement cost less depreciation. This may be due to poor location, bad neighborhood or economic obsolescence of the building. For example, in big cities, large homes in older residential areas often have a market value well below the replacement cost less depreciation. If a loss occurs, the fair market value may be used to determine the value of the loss. In one case, a building valued at $ 170,000 based on the actual cash value rule had a market value of only $ 65,000 when a loss occurred. The court ruled that the actual cash value of the property should be based on the fair market value of $ 65,000 rather than $ 170,000.

Broad Evidence Rule: The broad evidence rule means that the determination of actual cash value should include all relevant factors an expert would use to determine the value of the property. Relevant factors include replacement cost less depreciation, fair market value, present value of expected income from the property, comparison sales of similar property, opinions of appraisers and other factors. Although the actual cash value is used in property insurance, different procedures are followed for other types of insurance. In liability insurance, the amount paid for a loss is the actual damage the insured is legally obligated to pay because of badly injury or property damage to another. In business income insurance, the amount paid is usually based on the loss of profits plus continuing expenses incurred when the firm is shut down because of a loss from a covered period. In Life insurance, the amount paid upon the insured’s death is the face amount of the policy.

Exceptions to the principle of indemnity:

The important exceptions to the principle of indemnity are: Valued policy, Replacement cost insurance and Life Insurance

A valued policy is one that pays the face amount of insurance regardless of actual cash value if total loss occurs. They are used to insure fine arts & rare paintings. Because of difficulty in determining the actual cash value of the property at the time of loss, the insured and insurer both agree on the value of the property when the policy is first issued.(E.g. Old clock).

Replacement cost insurance means no deduction is taken for depreciation in determining the amount paid for a loss. For example, assume the roof on your home is 5 years old and has a useful life of 20 years. If the roof is damaged by a tornado, and the current cost of replacement is 10,000 birr. Under the actual cash value rule, you would receive only 7,500 birr (10,000 – 2,500 =7,500 birr). Under a replacement cost policy, you would receive the full 10,000 birr. Since you receive the value of a brand new roof instead of one that is 5 years old, the principle of indemnity is technically violated.

Life insurance is another exception to the principle of indemnity . A life insurance contract is not a contract of indemnity but it is avalued policy that pays a stated sum to the beneficiary upon the insured’s death. The indemnity principle is difficult to apply, because the historical actual cash value rule is meaningless in determining the value of a human life.

4.2 Principle of Insurable Interest

The principle of insurable interest states that the insured must lose financially if a loss occurs, or must incur some other kind of harm if the loss takes place. For example, a person has an insurable interest in his automobile, television or other property have been damaged or stolen.

Purposes of Insurable Interest

Insurable interest is essential in an insurance contract for the following reasons; First, an insurable interest is necessary to prevent gambling. If an insurable interest were not required, the contract would be a gambling contract and would be against the public interest. For example, one could insure the property of another and hope for an early loss. In the same way, one could insure the life of another and hope for an early death. Second, an insurable interest reduces moral hazard. If an insurable interest is not required, a dishonest person could purchase a property insurance contract on some one’s property and then deliberately cause a loss to receive the insurance claims. But, if the insured person stands to lose financially, nothing is gained by causing the loss.Thus, moral hazard is reduced.

Finally, an insurable interest measures the amount of the insured’s loss in property insurance; most contracts of property insurance are contracts of indemnity. Thus, the measure of recovery is the insurable interest of the insured. The amount of indemnification is measured by calculating the insurable interest in monetary terms. For example, if a person’s property worth 1 million Birr is insured and it was destroyed totally after some time, his insurable interest on that property depends on the financial loss met by him. Here, as the entire property is destroyed, his insurable interest tends to be 1 million Birr on that property. Thus, he will be indemnified the 1 million Birr.

When must an insurable interest exist?

In property insurance, the insurable interest must exist at the time of loss. There are two reasons for this requirement; First, most property insurance contracts are indemnity contracts. If an insurable interest did not exist at the time of loss, financial loss would not occur. For example, if Mr. X sells his car to Mr. Y, and it was stolen before the insurance on the car is cancelled, Mr. X cannot collect since he has no insurable interest on the car. Also Mr. Y cannot collect as he is not named as an insured under the policy. Second, one may not have an insurable interest in the property when the contract is first written, but may expect to have an insurable interest in the future, at the time of possible loss. For example, in a marine insurance, it is common to insure a return cargo by a contract entered into prior to the ship’s departure. However, the policy may not cover the goods until they are boarded on the ship as the insured’s property. Although an insurable interest does not exist when the contract is first written, one can still collect the claims if he has an insurable interest in the goods at the time of loss.

In life insurance contracts, the insurable interest requirement must be met only at the inception of the policy, not at the time of death. Life insurance is not a contract of indemnity, but it is valued policy that pays a stated sum upon the death of the insured. Since the beneficiary has only a legal claim to receive the policy proceeds, he need not show that a loss has been incurred by the insured’s death. For example, if Mrs. X has taken a policy on her husband Mr. X and later gets a divorce, she is entitled to the policy proceeds upon the death of her former husband if she has kept the insurance enforce.

4.3 Principle of Subrogation

Subrogation means substitution of the insurer in place of the insured for the purpose of claiming indemnity from a third person for a loss covered by insurance. This means that the insurer is entitled to recover from a negligent third party, any loss payments made to the insured. For example, assume that a negligent motorist smashes into Mr.X’s car, causing damages of 5,000 Birr. If Mr.X has the collision insurance on his car, his insurance company will pay 5,000 Birr and then attempt to collect from the negligent motorist who caused the accident. Alternatively, if Mr..X directly collect from the negligent motorist, the principle of subrogation does not apply because the loss payment is not made by the insurance company. However, to the extent that a loss payment is made, the insured gives to the insurer legal rights to collect damages from the negligent third party.

Purposes of Subrogation:

Subrogation has three basic purposes;

Subrogation prevents the insured from collecting twice for the same loss. In the absence of subrogation, the insured could collect from the insurer and from the person who caused the loss.

Subrogation is used to hold the guilty person responsible for the loss. By exercising its subrogation rights, the insurer can collect from the negligent person who caused the loss.

Subrogation tends to hold down insurance rates. Subrogation recoveries can be reflected in the rate making process, which tends to hold rates below where they would be in the absence of subrogation.

Note that:

The insured cannot impair the insurer’s subrogation rights; The insured cannot do anything that prejudices the insurer’s right to proceed against a negligent third party. For example, if the insured waives the right to sue the negligent party, the right to collect from the insurer for the loss is also waived.

The insurer can waive its subrogation rights in the contract; This may be to meet the special needs of some insured. For example, in order to rent an apartment house, a land lord may agree to release the tenants from potential liability if the building is damaged. If the land lord’s insurer waives its subrogation rights, and if a tenant negligently starts a fire, the insurer would have to reimburse the land lord for the loss, but could notrecover from the tenant since the subrogation rights were waived.

Subrogation does not apply to life insurance and to most individual health insurance contracts; Life insurance is not a contract of indemnity, and subrogation has relevance only for contracts of indemnity. Individual health insurance contracts usually do not contain subrogation clauses.

4.4 Principle of Utmost Good faith

Utmost good faith means that a higher degree of honesty is imposed on both parties to an insurance contract than is imposed on parties to other contracts. The principle of utmost good faith is supported by three important legal principles;

1.Representations

2.Concealment, and

3.Warranty

Representations: Representations are statements made by the applicant for insurance. For example, if a person wants to apply for life insurance, he may be asked questions concerning his age, weight, height, occupation, state of health and other relevant questions. The answers given by that person are called representations.

The legal importance of a representation is that the insurance contract is voidable at the insurer’s option if the representation is (a) false, (b) material and (c) relied on by the insurer.

False means that the statement given by the insured is not true or it is misleading. Material means that if the insurer knew the true facts, the policy would not have been issued, or would have been issued on different terms. Reliance means that the insurer relies on the misrepresentation in issuing the policy at the specified premium. For example, Mr. X may apply for life insurance and state in the application form that he has not visited a doctor within the last 5 years. But, he may have undergone surgery six months earlier. In this case, he has made a statement that is both false & material and the policy is voidable at the insurer’s option. Finally, an innocent or unintentional misrepresentation of a material fact, if relied on by the insurer also makes the contract voidable.

Concealment: Concealment is intentional failure of the applicant for insurance to reveal a material fact to the insurer. Here, the applicant for insurance deliberately withholds material information from the insurer. The legal effect of a material concealmentis also voidable at the insurer’s option. To deny a claim based on concealment, an insurer must prove two things:

The concealed fact was known by the insured and

The insured intended to defraud the insurer.

Warranty: The doctrine of warranty also reflects the principle of utmost good faith. A warranty is a statement of fact or promise made by the insured, which is part of the insurance contract and which must be true if the insured is to be liable under the contract. For example, in order to pay a reduced premium, the owner of a shop may warrant that an approved burglary and robbery alarm system will be operational at all times. The conditions describing the warranty become part of the contract.

4.5 Principle of Contribution

Contribution is the right of the insurer who has paid under a policy, to call upon other insurers equally or otherwise liable for the same loss to contribute to the payment. Where there is overinsurance because a loss is covered by policies effected with two or more insurers, the principle of indemnity still applies. In these circumstances the insured will only be entitled to recover the full amount of his loss and if one insurer has paidout in full, he will be entitled to nothing more. Like subrogation, contribution supports the principle of indemnity and applies only to contracts of indemnity. Therefore, there is no contribution in personal accident and life policies under which insurers contract to pay specific sums on the happening of certain events. Such policies are not contracts of indemnity, except to the extent that they may incorporate a benefit by way of indemnity, for example, payment of medical expenses incurred, in this respect contribution would apply.

Basis of Contribution

At the time of a claim, insurers usually inquire whether any other insurance exists covering the loss, where other insurances do exist and each policy is subject to a valid claim, contribution will apply so that the respective insurers share the loss ratably. That is insurers will pay proportionately to the coverage they have provided, in accordance with the following formula:

Share of Loss = (Particular Coverage / Total Coverage) x Indemnification

4.6 Principle of Proximate Cause

The rule is that immediate and not the remote cause is to be regarded. The maxim is “sed causa proxima non-remota spectatuture”, i.e., see the proximate cause and not the distant cause. The real cause must be seen while payment of the loss. If the real cause of loss is insured, the insurer is liable to compensate the loss; otherwise the insurer may not be responsible for loss. The efficient cause of a loss is called the proximate cause of the loss. For the policy to cover, the loss must have an insured peril as the proximate cause of the loss. The proximate cause is not necessarily the cause that was nearest to the damage, but is rather the cause that was actually responsible for loss; e.g. in marine insurance, seawater.

Determination of proximate cause

If there is a single cause of the loss, the cause will be the proximate cause and further if the peril (cause of loss) was insured, the insurer will have to indemnify the loss.

If there are concurrent causes, the insured perils and excepted perils have to be segregated. The concurrent causes may be separable or inseparable. Separable causes are those which canbe separated from each other. The loss occurred due to a particular cause may be clearly known. In such a case, if any cause is excepted peril, the insurer will have to pay up to the extent of loss which occurred due to insured perils. If the circumstances are such that the perils are inseparable, then the insurers are not liable at all when there is exists any excepted peril.

If the causes occurred in the form of chain, they have to be observed seriously.

If there is unbroken chain to excepted and insured perils, they have to be separated. If an excepted peril precedes the operation of the insured peril so that the loss caused by the insured peril is the direct and natural consequences of the excepted peril, there is no liability. If the insured peril is followed by an excepted peril there is valid liability.

If there is a broken chain of events with no excepted peril involved, it is possible to separate the losses. The insurer is liable only for the loss which is caused by an insured peril; when there is an excepted peril, the subsequent loss caused by an insured peril will be a new and indirect cause because of the interruption in the chain of events. Similarly, if the loss occurs by an insured peril and there is subsequently loss by an excepted peril, the insurer will be liable for loss occurred due to the insured peril.

Name: Anayo Bright Udochukwu

Reg Number: 2017/249482

Department: Economics

1. Foremost, when a company insures an individual entity there are basic legal requirement from both the insurer and insured. Thus, the legal principles of insurance are very fundamental for the smooth operations of insurance business and they clearly explain below

Indemnity: What is word stands in insurance coperative entity is the the insurance compensates the their customer i.e. the insured, of any damage of asset(s). A probability occurence that Mr Amadi insured his new sport utility vechicle of two months with a stipulate premium and after six the vehicle got stolen, hence, it is the duty of the insurance company to indemnify Mr Amadi on his lost vehicle. In other words replace Mr Amadi’s vehicle the way it is at the time of lost.

Insurable Interest: This legal principles explains that the insurer must have suffer from loss via the reason to get his asset(s) to be insured.

Utmost Good Faith: The insured must be able to explain to the insurer (insurance company) about asset to be insured and if any accidence occur, that the insured must be able to clearly state how it occured.

Contribution: There are certain situation where when the insure and insurer have to contribute in indemnify. A scenario where a vehicle was insured at the damage it may occur. Example dangote trucks.

Subrogation: This means that the insurance companies also work with para-millitary, military and other agencies in other to carry out their work effective. Example: In recovery of insured assets that was stolen like cars.

2. In an environment where there is so much antagonism towards insurance business, what my advice will be to an employee who works in an insurance company, and has been given a specific period of time to get a group of clients who will insure their assets/properties or even buy life assurance policies is that he/she should implore a convincing skill, say; giving insurance another name. An agent may come with a good statement to individuals who may not heard insurance before or other way, that he/she is an agent of a company that want to take away the lost occuring in your business for you thereby the person should be paying a little stipend monthly or annually.

3. Given the scenario above, assuming am the owner of the insurance firm. In other to get clients, i will rebrand the name of my insurance company. Train agents on marketing skills etc.

Name: Abiazia Rufus Chidiebube

Reg: 2017/243371

Dept: Economics

a. Principle of Indemnity: This principle states that the insurance company which is also called the insurer should restore the insured back to the position he or she was before the loss occurred given the insured’s premium. So whenever a client who wants to be insured or is already insured by an insurance company suffers a loss, that company should restore or rather indemnify its client back to the position he or she was in before the loss.

b. Principle of Insurable Interest: This principle states that whatever is to be covered or insured by the insurer should have a very big connection to the insured. That is, whatever thing be it property, or even a life as the case may be, the loss should be felt strongly by the insured.

c. Principle of Utmost Good Faith (Uberrima Fides): This principle states that everything information that would make the insurance policy be delivered by the insurance company which is the insurer and the insured should be disclosed between them both. That is, every information about the insured concerning the property or whatever is being insured should all be disclosed to the insurer.

d. Principle of Contribution: This principle states that insurance companies can come together to combine resources to indemnify a customer should in the case the companies have the same obligations to fulfill to the insured according to some stipulated methods.

2.

a. A good copywriting skills that will address the fear and introduce the comfort of getting ones business insured.

b. Enlightenment: education on the benefits of insurance, fidelity of the contemporary insurance company, and the easiness to get indemnify.

3

As the director, I will employ great copywriter, that can make use of scientific psychographical advertising strategies,

The company will be hosting seminar and invite business owner of the Institute New package of insurance .

7 principles of insurance

1. principle of indemnity: the principle of indemnity asserts that on the happening of a loss the insured shall be put back into the same financial position as he used to occupy immediately before the loss. In other words, the insured shall get neither more nor less than the actual amount of loss sustained.

2. principle of insurable interest: this concept requires that the insured have a stake in the loss or damage to the life or property insured

3. principle of utmost good faith: Here, the insurer and insured are bond by honesty and fairness

4. principle of contributions: insurers which have similar obligations to the insured contributes to the indemnification according to the same method

5. principle of subrogation: the insurance company acquires legal right to pursue recoveries on behalf of the insured

6. principle of cause proxima: here, the cause of loss must be covered under the insuring agreements

7. principle of mitigation: in case of any loss or damage, the assets owner must attempts to keep loss to minimum as though the item was not issured.

NO2

Employees who work in an insurance company and is seeking partnership, should firstly try to put on a friendly attitude and have a welcoming approach, secondly should enlighten people on the essence, advantage and usefulness of insurance in general. He or she can give incentives or discounts to attracts more people tpo the company.

NO3

As the manager to achieve 2 above, i will

1. be sincere from the start

2. discounts for new memberships

3. build a good customer relationship with my clients

4. more awareness

Ugwoke faith chinazaekpere

2017/249582

Economics

Question 1:

The basic principles of insurance include the following :

In the insurance world there are six basic principles that must be met, ie insurable interest, Utmost good faith, proximate cause, indemnity, subrogation and contribution.

1) lnsurable interest:

The right to insure arising out of a financial relationship, between the insured to the insured and legally recognized.

2) utmost good faith :

An action to disclose accurately and completely, all facts material (material fact) about something that will be insured is requested or not. The meaning is: the insurer must honestly explain everything clearly about the extent of the terms / conditions of the insurer and the insured must also provide a clear and correct for objects or interests of the insured.

3) proximate cause

is an active cause, efficient cause that chain of events that lead to a result without the intervention of the start and working actively from a new and independent.

4) indemnity :

One mechanism by which the insurer provides financial compensation to place the insured in a financial position that he had prior to the loss (Commercial code article 252, 253 and affirmed in section 278).

5) subrogation

Right transfer request from the insured to the insurer after a claim is paid.

6) contribution :

While the insurer the right to invite any other person equally bear, but do not have the same obligations to the insured to participate in providing indemnity.

Question 2

in my own opinion, I will try and offer some incentive, discount and probably offer them gift in order to get them to insure what ever they want and I will equally try to improve myself by possessing the right marketing skills in order convince them on what to do.

Question 3:

it can be done by getting a referrals system, running an advert on it online and employ the people that works for the company to grant incentive, with this you will able to motivate your target market to get insured.

NAME: MGBADA OGOCHUKWU EMELDA

REG NO:2017/245040

DEPARTMENT: ECONOMICS

Due to the high level of illiteracy in the Nigerian society, many people are unaware of insurance policies. However, with the enactment of Insurance Decree[1], the awareness of insurance policies was enhanced. Thus, more people took steps to insure their properties or lives. Unfortunately, however, much as the high percentage of them normally end up unable to have their claims indemnified, either as a result of a breach of one insurance principle or another. These principles are numerous and they are the basis upon which insurance contracts are based. Failure to adhere to any of the principles may render an insurance contract void. The need to understand as well as having a second knowledge of the basic principles of insurance cannot be over emphasized. In the insurance world there are six basic principles that must be met, ie insurable interest, Utmost good faith, proximate cause, indemnity, subrogation and contribution. The right to insure arising out of a financial relationship, between the insured to the insured and legally recognized.

1. Utmost Good Faith

2. Insurable Interest

3. Proximate Cause

4. Indemnity

5. Subrogation

6. Contribution

7. Loss Minimization

Below we explain each item briefly, including how each may relate to a potential injury lawsuit. These principles are open to interpretation. If you think one of these principles has been breached, or your insurance claim has wrongfully been denied, we recommend using our free case evaluation to help decide whether hiring a lawyer makes sense for you.

The Principle of Utmost Good Faith

• Both parties involved in an insurance contract—the insured (policy holder) and the insurer (the company)—should act in good faith towards each other.

• The insurer and the insured must provide clear and concise information regarding the terms and conditions of the contract

This is a very basic and primary principle of insurance contracts because the nature of the service is for the insurance company to provide a certain level of security and solidarity to the insured person’s life. However, the insurance company must also watch out for anyone looking for a way to scam them into free money. So each party is expected to act in good faith towards each other.

If the insurance company provides you with falsified or misrepresented information, then they are liable in situations where this misrepresentation or falsification has caused you loss. If you have misrepresented information regarding subject matter or your own personal history, then the insurance company’s liability becomes void (revoked).

See how a social media post could ruin a personal injury case.

The Principle of Insurable Interest

Insurable interest just means that the subject matter of the contract must provide some financial gain by existing for the insured (or policyholder) and would lead to a financial loss if damaged, destroyed, stolen, or lost.

• The insured must have an insurable interest in the subject matter of the insurance contract.

• The owner of the subject is said to have an insurable interest until s/he is no longer the owner.

In auto insurance, this will most times be a no brainer, but it does lead to issues when the person driving a vehicle doesn’t own it. For instance, if you are hit by a person who isn’t on the insurance policy of the vehicle, do you file a claim with the owner’s insurance company or the driver’s insurance company? This is a simple but crucial element for an insurance contract to exist.

The Principle of Indemnity

• Indemnity is a guarantee to restore the insured to the position he or she was in before the uncertain incident that caused a loss for the insured. The insurer (provider) compensates the insured (policyholder).

• The insurance company promises to compensate the policyholder for the amount of the loss up to the amount agreed upon in the contract.

Essentially, this is the part of the contract that matters the most for the insurance policyholder because this is the part of the contract that says she or he has the right to be compensated or, in other words, indemnified for his or her loss.

The amount of compensation is in direct proportion with the incurred loss. The insurance company will pay up to the amount of the incurred loss or the insured amount agreed on in the contract, whichever is less. For instance, if your car is inured for $10,000 but damages are only $3,000. You get $3,000 not the full amount.

Compensation is not paid when the incident that caused the loss doesn’t happen during the time allotted in the contract or from the specific agreed upon causes of loss (as you will see in The Principle of Proximate Cause). Insurance contracts are created solely as a means to provide protection from unexpected events, not as a means to make a profit from a loss. Therefore, the insured is protected from losses by the principle of indemnity, but through stipulations that keep him or her from being able to scam and make a profit.

The Principle of Contribution

• Contribution establishes a corollary among all the insurance contracts involved in an incident or with the same subject.

• Contribution allows for the insured to claim indemnity to the extent of actual loss from all the insurance contracts involved in his or her claim.

For instance, imagine that you have taken out two insurance contracts on your used Lamborghini so that you are covered fully in any situation. Let’s say you have a policy with Allstate that covers $30,000 in property damage and a policy with State Farm that cover $50,000 in property damage. If you end up in a wreck that causes $50,000 worth of damage to your vehicle. Then about $19,000 will be covered by Allstate and $31,000 by State Farm.

This is the principle of contribution. Each policy you have on the same subject matter pays their proportion of the loss incurred by the policyholder. It’s an extension of the principle of indemnity that allows proportional responsibility for all insurance coverage on the same subject matter.

The Principle of Subrogation

This principle can be a little confusing, but the example should help make it clear. Subrogation is substituting one creditor (the insurance company) for another (another insurance company representing the person responsible for the loss).

• After the insured (policyholder) has been compensated for the incurred loss on a piece of property that was insured, the rights of ownership of this property go to the insurer.

So lets say you are in a car wreck caused by a third party and your file a claim with your insurance company to pay for the damages on your car and your medical expenses. Your insurance company will assume ownership of your car and medical expenses in order to step in and file a claim or lawsuit with the person who is actually responsible for the accident (i.e. the person who should have paid for your losses).

The insurance company can only benefit from subrogation by winning back the money it paid to its policyholder and the costs of acquiring this money. Anything paid extra from the third party, is given to the policyholder. So lets say your insurance company filed a lawsuit with the negligent third party after the insurance company had already compensated you for the full amount of your damages. If their lawsuit ends up winning more money from the negligent third party than they paid you, they’ll use that to cover court costs and the remaining balance will go to you.

The Principle of Proximate Cause

• The loss of insured property can be caused by more than one incident even in succession to each other.

• Property may be insured against some but not all causes of loss.

• When a property is not insured against all causes, the nearest cause is to be found out.

• If the proximate cause is one in which the property is insured against, then the insurer must pay compensation. If it is not a cause the property is insured against, then the insurer doesn’t have to pay.

When buying your insurance policies, you will most likely go through a process where you select which instances you and your property will be covered for and which ones they will not. This is where you are selecting which proximate causes are covered. If you end up in an incident, then the proximate cause will have to be investigated so that the insurance company validates that you are covered for the incident.

This can lead to disputes when you have suffered an incident you thought was covered but your insurance provider says it’s not. Insurance companies want to make sure they are protecting themselves but sometimes they can use this to get out of being liable for a situation. This might be a dispute where you’ll need a lawyer to help argue for you.

The Principle of Loss Minimization

This is our final principle that creates an insurance contract and the most simple one probably.

• In an uncertain event, it is the insured’s responsibility to take all precautions to minimize the loss on the insured property.

Insurance contracts shouldn’t be about getting free stuff every time something bad happens. Therefore, a little responsibility is bestowed upon the insured to take all measures possible to minimize the loss on the property. This principle can be debatable, so call a lawyer if you think you are being unfairly judged under this principle.

HOW CAN A STAFF MEET THE TARGET

The main concept of insurance is that of spreading risks. Insurance facilitates investment by reducing the amount of capital that businesses and individuals need to keep at hand to protect themselves from uncertain events. According to some scholars, insurance is a barometer of economic activity in a country and thus, protects the success of emerging economies.

Insurance in Nigeria can be traced back to the 20th century when Nigeria’s economy was solely dependent on agriculture. There was a need for merchants to transport their cash crops to Europe and also reducing the risk of such transportation. This majorly contributed to the dominance of marine insurance in Nigeria at that time.

Despite its importance for economic development, the gross premium collected by insurance companies in Nigeria is about 1.9 Billion United States Dollars compared to the 3.8 Billion United States Dollars collected in South Africa.

In the United Kingdom, the insurance industry contributes about 20% of the total GDP of the country. In South Africa, the insurance industry contributes 17% of the total GDP and in Kenya, the insurance industry contributes 3.4% of its nation’s GDP. However, in spite the astronomical growth of the Insurance companies from just one agency in 1918 – Royal Exchange Assurance Agency to the present number of 56 Insurance companies as stated on National Insurance Commission (“NAICOM’s”) website, the Nigerian Insurance industry contributes a meagre 0.7% of the total GDP of Nigeria. It will be right to say that the performance of Nigerian insurance industry is sub-optimal.

In defiance of National Insurance Commission’s constant effort to cure and mitigate the challenges causing the sub-optimal performance of the insurance industry, there are still a couple of challenges militating against the growth of the insurance industry.

Antagonistic and hostile economy

A stable economy promotes the savings necessary to finance investments which is a prerequisite for achieving a viable insurance industry which can help sustain economic growth. Insurance companies are sensitive to economic fundamentals and sometimes have to factor a lot of economic variables so as to make the right investment decisions.

These variables include foreign exchange reserves, government debt, government deficits, inflation, interest rates and exchange rates which have all suffered in recent years as a result of Nigeria’s financial indiscipline and misappropriation.

What this means is that for the insurance industry to thrive and attain its potentials, the government must be sincere in promoting a favourable environment that will allow the financial service industries thrive. This will help increase the operational efficiency of the insurance industry.

Presently, insurance companies are unwilling to invest the premiums in long-term instruments because of the fear of inflation built up over several years due to fiscal indiscipline and high inflation. It is a very simple principle of economics and investment that short-term investment will yield lower returns. If these trend continues to occur, insurance companies will not be able to solve their liquidity problems which might deter insurers to pay claims.

The Nigerian market is doubtful of Insurance Companies

Anybody who has spoken to the average Nigerian about insurance can give a firsthand experience of how Nigerians generally have a negative attitude toward insurance. This accounts for the low patronage of insurance companies in Nigeria.

The negative attitude of Nigerians might not be unconnected to the poor attitude of the insurers as regards non-payment of claims. Some insurance companies are very notorious of defaulting in payment of claims which has adversely affected the publicity for the industry and consequently the confidence in the industry buy the prospective assured.

Also, there are clauses in policy documents which escalates the distrust in Nigerians.

Inadequate access to information Technology

Despite being in a world where information technology seems to be ruling everything, many companies in the insurance industry still do not have a fully automated and/or integrated computer software system. The challenge here is that document management system is relatively poor compared to other sectors in the economy.

It is an unfortunate truth that manual services are still prevalent in the industry which leads to delay in settlement of claims, fraudulent practices, mistakes and errors in the entire business operations.

There is also no regulatory guideline on best IT infrastructure for insurers and re-insurers to adopt for both operational and reporting purposes.

Weak Regulatory Framework

The regulatory framework for insurance is very weak. National Insurance Commission is empowered to ensure the effective administration, supervision, regulation and control of insurance business in Nigeria.

Historically in Nigeria, government policies and legislations were made concerning insurance industry simply to whittle down foreign dominance in the industry. There is an urgent need to review the laws regulating the Insurance industry. The Marine Insurance Act, 1961 is clearly outdated as it was a verbatim reproduction of the Marine Insurance Act 1906 of the United Kingdom which has been reviewed in the UK.

There is also a need for policies making some insurance products compulsory and mechanism to ensure full implementation of such policies. More stringent policies in relation to retaining more local content in some special risk such as aviation and oil& gas must be made by the legislators and National Insurance Commission.

Another major problem is National Insurance Commission inability to ensure that there are standard premium rates on certain insurance products. Insurance companies must adhere to the policy such that there is a benchmark for rates when negotiating premiums.

Lack of skilled personnel

As funny as it may seem, there is a huge shortfall of skilled professionals (underwriters, brokers, actuaries, etc.) in the entire insurance industry. Insurance companies inadequately train their staffs. Majority of the insurance companies attract low-skilled personnel due to inadequate remuneration package thus, there is always the inability to retain competent employees.

Many top executives in the insurance industry are marketers who have rose through the ranks not because of their strong technical background of the industry but because of their distinctive salesmanship and the ability to bring in more clients than the others. The author thinks bringing in client should be a major requirement of promotion, however, the combination of a good technical background and business skills should be the pre- requisite. Many marketers out there would give any rate to the prospective assured, not looking at important factors such as claims history and other major factors.

Poor knowledge of Insurance Services by the prospective assured

The insurance culture in Nigeria is very low. This may not be unconnected to the lack of knowledge about life insurance products. Many educated Nigerians still do not see a reason for insurance. Scholars have stated that there is an urgent need for insurance companies to renew their marketing communication strategy that should be based on creating awareness and informing the consumers of the benefits inherent to insurance.

Nigeria is a nation plagued with a low level of development, vast income inequalities,and cultural diversity in terms of language, religion, ethnicity and resource control crises.

The low standard of living is a major reason for the poor attitude of Nigerians towards insurance services. The per capital income in Nigeria is very low and thus insurance penetration into the economy is bound to be low.

Possible actions to ensure optimal operation of Insurance Industry in Nigeria

The Federal Government must also examine the extant legislations on insurance in Nigeria. Particularly the Insurance Act 2003 and the National Insurance Commission Act 1997. The Insurance Act must also be well implemented by NAICOM or any other government institution saddled with such implementation responsibility. For instance, Section 64 of the Insurance Act makes compulsory insurance of building under construction which is more than two floors. The general implementation of the Insurance Act has left more to be desired. The limitation of liability on third party insurance is too small in line with the present day economy. Several sections of the insurance Act have also been badly implemented. We cannot overemphasize the need for an adequate legislation and policy to create operational environment.

The formulation of economic policies which will give room for investment will also help the insurance industry. As earlier stated, where there are investment friendly policies, insurance companies would also be able to make long term investment for better returns on such investments. Also, it is noteworthy of stating that if the economy is in a better shape, the prospective assure will have the liquidity to procure insurance.

Customer services in the insurance industry is below par. Many of these companies are having problem satisfying their customers in terms of product offerings, quality of services and sophistication of products offered. Customer service is clearly important for winning new customers and retaining existing ones. The first step of changing the face of the industry is ensuring an exceptional customer experience. Insurance companies must find a way to provide customers with a internet based self-service insurance platform where customers can view policy coverage, pay bills, make changes to policies, submit claims and check the status of claim progress. Brokers should be able to obtain online quotes, proposal and plans, design for their customers.

Employing more adequate staff with related professional background is also key. It is also important that the Chartered institute of Insurance must regularly review and expand their curriculum to meet with the present market need and build the capacity of student members. Insurance companies must also allocate a percentage of its budget to Continuous Professional Development to keep staff abreast of professional standards and practices.

Insurance companies must also find ways to sensitise the populace about the use of insurance. The government also has a role to play in this by making relevant laws that will help make certain insurance policies compulsory and harsh sanctions for non-compliance of same.

Generally, around the world, there is a paradigm shift from paper oriented process which is manual to automated process. Insurance companies in Nigeria must follow this growing trend. Insurance companies must employ the expertise of first tier technology firms to develop software to increase operational efficiency.

ways to get more clients for your insurance business

1. Find your niche. Insurance agents often want to be all things to all people, but niche marketing may be the smarter strategy. …

2. Network in your community. You already know that networking is essential for bringing in new clients. …

3. Prospect every day. …

4. Partner with other professionals. …

5. Nurture your leads.

Name: Ijara Peter Elochukwu

Department: ECONOMICS

Reg no: 2017/ 249513

EMAIL: petochris86@yahoo.com

Eco 324.

1.

There are 7 principles guiding the operation of the insurance company. They include.

I. Indemnity: in cases of loss a policy holder is expected to be restored to his or her previous status before the loss. If I lose my insure my car I expect to be restored to my original position before the loss.

II. Insurable interest: it’s imperative to note that one cannot insure something that if a loss happen that certain thing won’t affect them directly.

III. Utmost good faith: at this point both parties are honest with each other and disclosed all information relevant for the policy. If I want a life insurance then I have to reveal information about my health.

IV. Mitigation: in this case policy holders are expected to take care of insured property like it wasn’t insured. If you insured your house doesn’t mean you’ll stop taking measures to prevent fire and other man made disaster .

V. Contribution: insurers who have similar obligation to the insured contribute to indemnify the loss through special methods

VI. Causa proxima: The cause of loss must be covered under the insuring agreement of the policy and the dominant cause must not be excluded.

VII. Subrogation: This principle states that the insurance company has rights to pursue whatever concerns the insured on behalf on the insured.

The insurance business been a profit oriented one has a business model that collects more in premium thanks paid out in losses.

1. Underwriting: The process where the insurers select risk to insure and premium to collect for accepting the risks.

2. Through investing of premiums.

Question 2

I. Ask of the potential clients wellbeing:studies reveed that more clients will buy insurance policies if their wellbeing is considered.

II. Highlighting the advantages of a product or service offered by your company is very important.

III. Act on their emotions.

IV. Make clients feel they are missing out of they don’t purchase insurance policies. It’s called the FOMO effect.

V. Let your customers decide on the next steps: don’t decide for them so they don’t think all you are after is just the sale of your insurance policy.

VI. Use the internet to display times the company indemnify it’s clients in time of loss. This helps to restore loss confidence.

Question 3.

I. Encouraging sales person with bounces for meeting a target

2. Emotional intelligence classes for sales persons.

3. Proof of insurance companies loyalty.

Name: Ijara Peter Elochukwu

Department: ECONOMICS

Reg no: 2017/ 249513

EMAIL: petochris86@yahoo.com

Eco 324.

1.

There are 7 principles guiding the operation of the insurance company. They include.

I. Indemnity: in cases of loss a policy holder is expected to be restored to his or her previous status before the loss. If I lose my insure my car I expect to be restored to my original position before the loss.

II. Insurable interest: it’s imperative to note that one cannot insure something that if a loss happen that certain thing won’t affect them directly.

III. Utmost good faith: at this point both parties are honest with each other and disclosed all information relevant for the policy. If I want a life insurance then I have to reveal information about my health.

IV. Mitigation: in this case policy holders are expected to take care of insured property like it wasn’t insured. If you insured your house doesn’t mean you’ll stop taking measures to prevent fire and other man made disaster .

V. Contribution: insurers who have similar obligation to the insured contribute to indemnify the loss through special methods

VI. Causa proxima: The cause of loss must be covered under the insuring agreement of the policy and the dominant cause must not be excluded.

VII. Subrogation: This principle states that the insurance company has rights to pursue whatever concerns the insured on behalf on the insured.

The insurance business been a profit oriented one has a business model that collects more in premium thanks paid out in losses.

1. Underwriting: The process where the insurers select risk to insure and premium to collect for accepting the risks.

2. Through investing of premiums.

Question 2

I. Ask of the potential clients wellbeing:studies reveed that more clients will buy insurance policies if their wellbeing is considered.

II. Highlighting the advantages of a product or service offered by your company is very important.

III. Act on their emotions.

IV. Make clients feel they are missing out of they don’t purchase insurance policies. It’s called the FOMO effect.

V. Let your customers decide on the next steps: don’t decide for them so they don’t think all you are after is just the sale of your insurance policy.

VI. Use the internet to display times the company indemnify it’s clients in time of loss. This helps to restore loss confidence.

Question 3.

I. Encouraging sales person with bounses for meeting a target

2. Emotional intelligence classes for sales persons.

3. Proof of insurance companies loyalty.

NAME: IJE VORDA GOODNESS

DEPARTMENT: ECONOMICS

REG NO: 2017/249514

EMAIL: vordagoodness78@gmail.com

COURSE: ECO 324

Question 1

Indemnity: The insurance firms are expected to indemnify the insured in case of loss to the extent the interest. If Amaka insured her car them in case of fire outbreak Amaka is expected to indemnified i.e retired so she has her car again.

Indemnity: The insurance firms are expected to indemnify the insured in case of loss to the extent the interest. If Amaka insured her car them in case of fire outbreak Amaka is expected to indemnified i.e retired so she has her car again.

Insurable interest: the insured must directly affect the insured. This simply means that a person can’t insure something that won’t directly affect to them in case of loss. I can’t insure another person’s car because in the loss of the car I won’t be directly affected. The person insuring must have a stake in the insured property.

Insurable interest: the insured must directly affect the insured. This simply means that a person can’t insure something that won’t directly affect to them in case of loss. I can’t insure another person’s car because in the loss of the car I won’t be directly affected. The person insuring must have a stake in the insured property.

Utmost good faith: the insured and the insurer are bound by a good faith of honestly and fairness. Materials fact must be disclosed. If I want to buy a health insurance policy I have to reveal to the insurer all underlining health conditions and Health conditions.

Utmost good faith: the insured and the insurer are bound by a good faith of honestly and fairness. Materials fact must be disclosed. If I want to buy a health insurance policy I have to reveal to the insurer all underlining health conditions and Health conditions.

Contribution: insurers who have similar obligation to the insured contribute to indemnify the loss through special methods.

Contribution: insurers who have similar obligation to the insured contribute to indemnify the loss through special methods.

Subrogation: the insurance company has a right to sue anybody responsible for the loss of insured . If for Nkechi car is stole by armed robbers and the vehicle is insured, the insurance company can undertake a search process for the vehicle and punish offenders.

Subrogation: the insurance company has a right to sue anybody responsible for the loss of insured . If for Nkechi car is stole by armed robbers and the vehicle is insured, the insurance company can undertake a search process for the vehicle and punish offenders.

Proximate cause: the cause of the loss must be covered under the insuring agreement of the policy.

Proximate cause: the cause of the loss must be covered under the insuring agreement of the policy.

Mitigation: in case of loss the asset owner must try to keep lossat a minimum like the property is not insured. If you insure your house and suddenly there’s a fire outbreak try putting out the fire so more damage is done to the building.

Mitigation: in case of loss the asset owner must try to keep lossat a minimum like the property is not insured. If you insure your house and suddenly there’s a fire outbreak try putting out the fire so more damage is done to the building.

Insurance firms as we all know perform the function of accepting risks for an agreed premium payable by the insured. They are however 7 principle guilding the insurance business.

They are:

Insurance companies a profit making venture therefore adopt a business model that ensures it gets more premium than it’s paying out in losses.

1. Underwriting: in this case insurance companies decide what risks to accept and how much should be paid as premium on that risk.

2. Investing premium left after indemnity every year.

Question 2

Act on your clients emotions and tell them how important they are to you and the insurance company.

Act on your clients emotions and tell them how important they are to you and the insurance company.

Leverage on the power FOMO: when you have told your clients about your value added products. Let them feel they are missing out if they don’t purchase your insurance policy.

Leverage on the power FOMO: when you have told your clients about your value added products. Let them feel they are missing out if they don’t purchase your insurance policy.

let your clients decide for themselves so you don’t send the signal of been pushy.

let your clients decide for themselves so you don’t send the signal of been pushy.

However in a country like Nigeria, so many people are skeptical about purchasing insurance policies due to why they have heard and experience themselves with insurance companies. How then do you convince them that your insurance policy is genuine and they should buy?…the following are a few tips.

1. Don’t act like a robot! Don’t read from a script to the client because it gives the subtle impression that you don’t really care but is just there for sales.Customers are more willing to buy if they establish an emotional relationship with a consultant.

2. Ask about the well-being of those you want to sell policies to. Studies have shown that the probability of selling and insurance policy increased a great deal.

3. When talking to a client learn their names:

Psychological research shows that people like to hear their name and are much more likely to make a friendly relationship when the other side uses it.

4. You must prove that your insurance policy is better than that of your competitors and ensure your genuine with proof. To further push this insurance companies can leverage on the power of the internet by posting on line the proof when the indemnify.

Question 3

Improvement in insurance product and Insurance company should Leverage on the internet to popularised when they indemnify someone.

Improvement in insurance product and Insurance company should Leverage on the internet to popularised when they indemnify someone.