A financial system makes it possible for investors, lenders and borrowers to interact with each other. This system is mainly divided into financial institutions, markets, instruments and services. These parts help to ensure economic growth and development by ensuring that money is circulated to all sectors of the economy. Discuss

REG NO: 2017/249521

DEPT: ECONOMICS

What Are Financial Markets?

Financial markets refer broadly to any marketplace where the trading of securities occurs, including the stock market, bond market, forex market, and derivatives market, among others. Financial markets are vital to the smooth operation of capitalist economies.

Understanding the Financial Markets:

Financial markets play a vital role in facilitating the smooth operation of capitalist economies by allocating resources and creating liquidity for businesses and entrepreneurs. The markets make it easy for buyers and sellers to trade their financial holdings. Financial markets create securities products that provide a return for those who have excess funds (Investors/lenders) and make these funds available to those who need additional money (borrowers).

The stock market is just one type of financial market. Financial markets are made by buying and selling numerous types of financial instruments including equities, bonds, currencies, and derivatives. Financial markets rely heavily on informational transparency to ensure that the markets set prices that are efficient and appropriate. The market prices of securities may not be indicative of their intrinsic value because of macroeconomic forces like taxes.

Some financial markets are small with little activity, and others, like the New York Stock Exchange (NYSE), trade trillions of dollars of securities daily. The equities (stock) market is a financial market that enables investors to buy and sell shares of publicly traded companies. The primary stock market is where new issues of stocks, called initial public offerings (IPOs), are sold. Any subsequent trading of stocks occurs in the secondary market, where investors buy and sell securities that they already own.

Prices of securities traded in the financial markets may not necessarily reflect their true intrinsic value.

Types of Financial Markets

Stock Markets

Perhaps the most ubiquitous of financial markets are stock markets. These are venues where companies list their shares and they are bought and sold by traders and investors. Stock markets, or equities markets, are used by companies to raise capital via an initial public offering (IPO), with shares subsequently traded among various buyers and sellers in what is known as a secondary market.

Stocks may be traded on listed exchanges, such as the New York Stock Exchange (NYSE) or Nasdaq, or else over-the-counter (OTC). Most trading in stocks is done via regulated exchanges, and these play an important role in the economy as both a gauge of the overall health in the economy as well as providing capital gains and dividend income to investors, including those with retirement accounts such as IRAs and 401(k) plans.

Typical participants in a stock market include (both retail and institutional) investors and traders, as well as market makers (MMs) and specialists who maintain liquidity and provide two-sided markets. Brokers are third parties that facilitate trades between buyers and sellers but who do not take an actual position in a stock.

Over-the-Counter Markets

An over-the-counter (OTC) market is a decentralized market—meaning it does not have physical locations, and trading is conducted electronically—in which market participants trade securities directly between two parties without a broker. While OTC markets may handle trading in certain stocks (e.g., smaller or riskier companies that do not meet the listing criteria of exchanges), most stock trading is done via exchanges. Certain derivatives markets, however, are exclusively OTC, and so make up an important segment of the financial markets. Broadly speaking, OTC markets and the transactions that occur on them are far less regulated, less liquid, and more opaque.

Bond Markets

A bond is a security in which an investor loans money for a defined period at a pre-established interest rate. You may think of a bond as an agreement between the lender and borrower that contains the details of the loan and its payments. Bonds are issued by corporations as well as by municipalities, states, and sovereign governments to finance projects and operations. The bond market sells securities such as notes and bills issued by the United States Treasury, for example. The bond market also is called the debt, credit, or fixed-income market.

Money Markets

Typically the money markets trade in products with highly liquid short-term maturities (of less than one year) and are characterized by a high degree of safety and a relatively low return in interest. At the wholesale level, the money markets involve large-volume trades between institutions and traders. At the retail level, they include money market mutual funds bought by individual investors and money market accounts opened by bank customers. Individuals may also invest in the money markets by buying short-term certificates of deposit (CDs), municipal notes, or U.S. Treasury bills, among other examples.

Derivatives Markets

A derivative is a contract between two or more parties whose value is based on an agreed-upon underlying financial asset (like a security) or set of assets (like an index). Derivatives are secondary securities whose value is solely derived from the value of the primary security that they are linked to. In and of itself a derivative is worthless. Rather than trading stocks directly, a derivatives market trades in futures and options contracts, and other advanced financial products, that derive their value from underlying instruments like bonds, commodities, currencies, interest rates, market indexes, and stocks.

Futures markets are where futures contracts are listed and traded. Unlike forwards, which trade OTC, futures markets utilize standardized contract specifications, are well-regulated, and utilize clearinghouses to settle and confirm trades. Options markets, such as the Chicago Board Options Exchange (CBOE), similarly list and regulate options contracts. Both futures and options exchanges may list contracts on various asset classes, such as equities, fixed-income securities, commodities, and so on.

Forex Market

The forex (foreign exchange) market is the market in which participants can buy, sell, hedge, and speculate on the exchange rates between currency pairs. The forex market is the most liquid market in the world, as cash is the most liquid of assets. The currency market handles more than $5 trillion in daily transactions, which is more than the futures and equity markets combined. As with the OTC markets, the forex market is also decentralized and consists of a global network of computers and brokers from around the world. The forex market is made up of banks, commercial companies, central banks, investment management firms, hedge funds, and retail forex brokers and investors.

Commodities Markets

Commodities markets are venues where producers and consumers meet to exchange physical commodities such as agricultural products (e.g., corn, livestock, soybeans), energy products (oil, gas, carbon credits), precious metals (gold, silver, platinum), or “soft” commodities (such as cotton, coffee, and sugar). These are known as spot commodity markets, where physical goods are exchanged for money.

The bulk of trading in these commodities, however, takes place on derivatives markets that utilize spot commodities as the underlying assets. Forwards, futures, and options on commodities are exchanged both OTC and on listed exchanges around the world such as the Chicago Mercantile Exchange (CME) and the Intercontinental Exchange (ICE).

Cryptocurrency Markets

The past several years have seen the introduction and rise of cryptocurrencies such as Bitcoin and Ethereum, decentralized digital assets that are based on blockchain technology. Today, hundreds of cryptocurrency tokens are available and trade globally across a patchwork of independent online crypto exchanges. These exchanges host digital wallets for traders to swap one cryptocurrency for another, or for fiat monies such as dollars or euros.

Because the majority of crypto exchanges are centralized platforms, users are susceptible to hacks or fraud. Decentralized exchanges are also available that operate without any central authority. These exchanges allow direct peer-to-peer (P2P) trading of digital currencies without the need for an actual exchange authority to facilitate the transactions. Futures and options trading are also available on major cryptocurrencies.

Examples of Financial Markets

The above sections make clear that the “financial markets” are broad in scope and scale. To give two more concrete examples, we will consider the role of stock markets in bringing a company to IPO, and the role of the OTC derivatives market in the 2008-09 financial crisis.

Stock Markets and IPOs

When a company establishes itself, it will need access to capital from investors. As the company grows it often finds itself in need of access to much larger amounts of capital than it can get from ongoing operations or a traditional bank loan. Firms can raise this size of capital by selling shares to the public through an initial public offering (IPO). This changes the status of the company from a “private” firm whose shares are held by a few shareholders to a publicly-traded company whose shares will be subsequently held by numerous members of the general public.

The IPO also offers early investors in the company an opportunity to cash out part of their stake, often reaping very handsome rewards in the process. Initially, the price of the IPO is usually set by the underwriters through their pre-marketing process.

Once the company’s shares are listed on a stock exchange and trading in it commences, the price of these shares will fluctuate as investors and traders assess and reassess their intrinsic value and the supply and demand for those shares at any moment in time.

How Do Financial Markets Work?

Despite covering many different asset classes and having various structures and regulations, all financial markets work essentially by bringing together buyers and sellers in some asset or contract and allowing them to trade with one another. This is often done through an auction or price-discovery mechanism.

What Are the Main Functions of Financial Markets?

Financial markets exist for several reasons, but the most fundamental function is to allow for the efficient allocation of capital and assets in a financial economy. By allowing a free market for the flow of capital, financial obligations, and money the financial markets make the global economy run more smoothly while also allowing investors to participate in capital gains over time.

Why Are Financial Markets Important?

Without financial markets, capital could not be allocated efficiently, and economic activity such as commerce & trade, investment, and growth opportunities would be greatly diminished.

Who Are the Main Participants in Financial Markets?

Firms use stock and bond markets to raise capital from investors; speculators look to various asset classes to make directional bets on future prices; hedgers use derivatives markets to mitigate various risks, and arbitrageurs seek to take advantage of mispricings or anomalies observed across various markets. Brokers often act as mediators that bring buyers and sellers together, earning a commission or fee for their services.

Name: Ijara Peter Elochukwu

Reg no: 2017/249513

EMAIL: petochris86@yahoo.com

Department: Economics

Financial institutions perform various functions in the econmy. One of which is financial intermediation, this is done through the transfer of funds from those who have excess to those in deficit and immediate need of funds for investment i.e net borrowers. Financial institutions therefore helps in the transfer of these funds from the savers to the borrowers.

Borrowers will not know the net savers.

Borrowers will not know the net savers.

Those with excess funds may lack trust in the investors. Since customers trust the financial intermediaries, they keep their idle funds with them, the financial intermediaries promise net savers to pay them whenever they need the money.

Those with excess funds may lack trust in the investors. Since customers trust the financial intermediaries, they keep their idle funds with them, the financial intermediaries promise net savers to pay them whenever they need the money.

The amount of funds needed by an investor may be too much for a saver or few savers to provide. Since financial institutions have access to the funds of numerous savers pooled together they lend to investors on behalf of net savers.

The amount of funds needed by an investor may be too much for a saver or few savers to provide. Since financial institutions have access to the funds of numerous savers pooled together they lend to investors on behalf of net savers.

Without financial institution the role of financial intermediation will be impossible since

Note that this funds are lended to investors at a price called interest rate which they use to generate extra credit in the economy to boost economic growth. They also give a part of the interest to the net savers to encourage them to save more of their excess funds. Before investors are given loans the viability of business is examined so that lenders are able to repay loans.

The loan given to these investors help in generating employment and productivity which leads to increase in the level of income and output (GDP) in a country.

Moreover financial institutions are instrumental in carrying out the monetary policies of the government that help in stabilizing the economy.

Therefore, the importance of financial institutions cannot be over emphasized.

Name: Edochie Praise Ifeoma

Reg no: 2017/249492

Email address: Edochie80@gmail.com

The different parts of the financial system interact together to move the economy forward. This financial participants ensure that excess funds are channelled from the people with excess money( savers) to those in need of this money ( net borrowers) this function carried out is called financial intermediation.

Now without financial institutions it will be very difficult to channel these funds for various reasons like lack of trust between borrowers and lenders, borrowers may not even know net savers and a single saver may not be able to supply all the funds needed. However the parts of the financial system make it possible to access large funds.

When savers put their excess funds in financial institutions they don’t remain idle funds instead these institutions channel it to investors for productive activities and not only that they charge interest on loans. Note that part of this interest are remitted to those savers to encourage them to save more funds that will be channelled to investment thereby boosting economic growth and development.

Financial institutions also give loans for productive ventures only and issue project specific loans to boost development. If the government of a country wants to boost growth and development it can also use financial institutions to do that by issuing specific loans to boost agriculture, industries, service sectors etc. The importance of financial institutions in economic growth and development cannot be overstated.

Name: Edochie Praise Ifeoma

Reg no: 2017/249492

Economics department

Email address: Edochie80@gmail.com

The different parts of the financial system interact together to move the economy forward. This financial participants ensure that excess funds are channelled from the people with excess money( savers) to those in need of this money ( net borrowers) this function carried out is called financial intermediation.

Now without financial institutions it will be very difficult to channel these funds for various reasons like lack of trust between borrowers and lenders, borrowers may not even know net savers and a single saver may not be able to supply all the funds needed. However the parts of the financial system make it possible to access large funds.

When savers put their excess funds in financial institutions they don’t remain idle funds instead these institutions channel it to investors for productive activities and not only that they charge interest on loans. Note that part of this interest are remitted to those savers to encourage them to save more funds that will be channelled to investment thereby boosting economic growth and development.

Financial institutions also give loans for productive ventures only and issue project specific loans to boost development. If the government of a country wants to boost growth and development it can also use financial institutions to do that by issuing specific loans to boost agriculture, industries, service sectors etc. The importance of financial institutions in economic growth and development cannot be overstated.

Okaome Esther Chioma

2017/249554

estherokaome@gmail.com

Good day Mr President and honourable members of the house

If a financial institutions enters Into a bankruptcy such as when the value of the banks assest falls below the market value of the bank liabilities because of the controversial practices by the financial institution, this would definitely leasd to a wide spread of economic disability and also after panic as people who have their money and valuables in the bank would begin to doubt the safety of their finances( money and other valuables) that are been kept in the financial markets.

This will obviously lead to or cause a negative externalies in the sense that the individual s would likely withdraw their money and other valuables they have in the bank , doing so this will now lead to loss of customers for that financial institution and it will not definitely affect the financial operations of the financial institution and would therefore affect the economy as a whole.

Some of the challenges of the financial institutions are:cost, lack of awareness and regulatory requirements, lack of robust technlogy.

Okaome Esther Chioma

2017/249554

estherokaome@gmail.com

What Are Financial Markets?

Financial markets refer broadly to any marketplace where the trading of securities occurs, including the stock market, bond market, forex market, and derivatives market, among others, financial markets refer broadly to any marketplace where the trading of securities occurs.There are many kinds of financial markets, including (but not limited to) forex, money, stock, and bond markets.

These markets may include assets or securities that are either listed on regulated exchanges or else trade over-the-counter (OTC)

Economic system relies heavily on financial resources and transactions, and economic efficiency rests in part on efficient financial markets. Financial markets consist of agents, brokers, institutions, and intermediaries transacting purchases and sales of securities. The many persons and institutions operating in the financial markets are linked by contracts, communications networks which form an externally visible financial structure, laws, and friendships. The financial market is divided between investors and financial institutions.

Types of financial markets

Stock market, commodity market, derivative market, bond market, investment market, money market e.t.c

Main Functions of Financial Markets?

Financial markets exist for several reasons, but the most fundamental function is to allow for the efficient allocation of capital and assets in a financial economy. By allowing a free market for the flow of capital, financial obligations, and money the financial markets make the global economy run more smoothly while also allowing investors to participate in capital gains over time, Without financial markets, capital could not be allocated efficiently, and economic activities.

NAME: OKOYE AMBLESSED AMARACHI

REG NO: 2017/249560

DEPT:ECONOMICS

FINANCIAL MARKETS AND INSTITUTIONS

A financial market is a trade center where financial securities(such as stocks and bonds) and other valuables can be bought and sold.

They are targeted at raising capital, transferring risks, facilitating global transactions as well as enabling the transfer of liquidity. The financial market bridges the gap between those who want capital and those who have this capital.

Its made up of the primary and secondary markets.

A financial institution is an entity that oversees financial transactions such as investment loans and deposits. They are but not limited to commercial banks, trust companies as well as investment dealers. These financial institutions are regulated by a number officials; they include: CBN, SEC, NDIC etc.

Chigbata Franklin Chigozie

2017/242424

Economics

Franklin.chigbata.242424@unn.edu.ng

Financial markets are the centers or an arrangement that provide facilities for buying and selling of financial claims and services the corporations, financial institutions, individuals and governments trade in financial products in these markets either directly or through brokers and dealers on organized exchanges or off-exchanges. The participants on the demand and supply sides of these markets are financial institutions, agents, brokers, dealers, borrowers, lenders, savers, and others who are interlinked by the laws, contracts, covenants and communication networks.

The primary markets deal in the new financial claims or new securities and, therefore, they are also known as new issue markets. On the other hand, secondary markets deal in securities already issued or existing or outstanding. The primary markets mobilize savings and supply fresh or additional capital to business units. Although secondary markets do not contribute directly to the supply of additional capital, they do so indirectly by rendering securities issued on the primary markets liquid. Stock markets have both primary and secondary market segments.

Name: ASOGWA Arinze GODWIN

Reg no: 2016/235173

Department: Economics

Financial system The structure of the Nigerian financial system could be viewed from the side of institutions and structures planted for the realization of basic goals of financial intermediation. The institutions in question operate in the financial market. Here their ultimate role is to facilitate the mobilization of funds from the surplus units (savers) to the deficit units (investors). The sweetener is interest income that makes the surplus units (savers) to transfer their purchasing power to the deficit units (investors).This what is called actual resources flow from lenders to borrowers Through this the production of goods and services is improved which also reflects on the aggregate output of our Nation. The institutions in the Nigerian financial system are as shown below:

1. The monetary authorities or regulators

2. The Presidency

3. Federal Ministry of Finance

4. The Central Bank of Nigeria (CBN) as the apex regulatory body in the financial system.

5. Institutions that provide long term funds or capital market operators,

6. Securities and Exchange Commission as the apex regulatory body

7. The stock exchange as the facilitator of trading in various listed securities

8. Development or Specialized financial institutions: they include: Bank of Industry, Nigerian Agricultural and cooperative Bank, Nigerian Bank for Commerce and Industry, Federal Mortgage Bank of Nigeria.

The financial system consists of various financial institutions, operators and Instruments that gives the system its character and uniqueness. According to the Central Bank of Nigeria research series (1993) the Nigerian financial system refers to a set of rules and regulations and the aggregation of financial arrangements, institutions, agents, that interact with each other and the rest of the world to foster economic growth and development of a nation. A national financial system differs from the Global Financial System (GFS). The Global Financial System (GFS) is a financial system consisting of institutions and regulations that act on the international level, as opposed to those that act on a national or regional level. The main players are the global Institutions, such as International Monetary Fund and Bank for International etc. The financial system is a prime mover of economic development. It achieves this through the intermediation process, which entails providing a medium of exchange necessary for specialization and the mobilization of savings from surplus units to deficit units.

Basic characteristics of the financial system

1. A high level of confidence must be in place in the system.

2. An efficient financial system must be able to sustain the intermediation process.

3. An efficient financial system must have in place a large number of intermediaries and participants who must stand ready to engage in healthy competition amongst themselves and within confines and boundaries specified by law and the various professional standards in place for the participants.

4. There should be a high degree of flexibility in the market. Also, the instruments (financial assets) employed and the methods of operation should be market based, so that the market can respond and adapt to changes in the economic and financial structure, no matter how small the change may be.

5. An efficient financial system must allow for balance in operations of the market. It requires that there should be an optimal mix of various types of financial institutions with respect to both the transfer of current savings and the stock the past savings.

The financial system plays the vital role of improvement and sustains the efficient mobilization and allocation of financial resources in an economy. The Financial system also provides structures for the management of liquidity for financial assets and instruments The Report on the Nigeria system (1976) succinctly articulated the functions of the financial system.

NAME: Anachuna Cynthia Chisom

REG NO:2017/249481

EMAIL:chisomcynthia4247@gmail.com

Financial Markets help to efficiently direct the flow of savings and investments in the Economy in ways that facilitate the accumulation of capital and the production of goods and services. Increase in productivity will lead to economic growth.

An efficient financial system correlate to a sustainable economic growth. The financial system mobilizes the savings, the financial system accept deposits in form of savings. And they lend funds to investors and business men, by making funds available to businesses, this encourages Businesses to expand, by expanding, they will employ more workers, and by employing more workers they increase productivity in the country thereby raising the country’s GDP(Economic growth).

Also, by increasing employment, they help to improve/increase the standard of living of the citizens of the country. Thereby promoting economic development.

Name: Ugochukwu Onyinyechi Marycynthia

Reg no: 2017/249580

Department: Economics

FINANCIAL SYSTEM- The financial system consists of various financial institutions, operators and Instruments that gives the system its character and uniqueness. According to the Central Bank of Nigeria research series (1993) the Nigerian financial system refers to a set of rules and regulations and the aggregation of financial arrangements, institutions, agents, that interact with each other and the rest of the world to foster economic growth and development of a nation. A national financial system differs from the Global Financial System (GFS). The Global Financial System (GFS) is a financial system consisting of institutions and regulations that act on the international level, as opposed to those that act on a national or regional level. The main players are the global Institutions, such as International Monetary Fund and Bank for International etc. The financial system is a prime mover of economic development. It achieves this through the intermediation process, which entails providing a medium of exchange necessary for specialization and the mobilization of savings from surplus units to deficit units. Through this process, there is an enhanced productive activity and thus positively influences aggregate output and economic growth. It means the system ensures the efficient transfer of savings from those who generate them (savers) to those who ultimately use them (investors) for investment or consumption. Well-functioning financial markets are an essential part of any modern healthy economy. It is through these markets that funds are offered by the lenders/savers who have excess funds and purchased by the borrowers/spenders who need those funds. The financial system also provides avenue for organizing and managing the payments system, mechanisms for the collection and transfer of savings by banks and other depository institutions; arrangements covering the activities of capital markets with respect to the issue and trading of long term securities, arrangement covering the workings of the money market in respect of short-term financial instruments; and arrangements covering the activities of financial markets complementary to the money and capital markets for example the foreign exchange market, the arrangements for risk insurance; the futures market etc. Nzotta (1999)

Empirical evidence shows that the level of financial system development in any nation is the best indicator of general economic development potential. Goldsmith (1969), for instance posits that financial system development is of prime importance because the financial superstructure, in the form of both primary and secondary securities, accelerates economic growth and improves economic performance, to the extent that it facilitates the migration of funds to the best user i.e. to the place in the economic system where the funds will yield the highest social return. The implication here is that the financial system will discriminate against inefficient funds users. In helping as a vehicle to economic development, the financial system tries to achieve the basic function of resource intermediation. Here, through various institutional structures, they vigorously seek out and attract the reservoir of idle funds and allocate same to entrepreneurs, businesses, households and governments, for investments and use in various projects and purposes, with a view of returns. Alternatively, they may listlessly exploit their quasi-monopolistic position and fritter away investment possibilities with unproductive loans (investments).Cameroon et al (1969). It is therefore an axiom that without financial wherewithal, no business enterprise (small, medium, or big) or government can perform its productive functions effectively and efficiently. Consequently, financial resources affect business development.

FUNCTION OF FINANCIAL SYSTEM

1. Facilitate effective management of the economy;

2. Provide non inflationary support to the economy;

3. Achieve greater mobilization of savings and its efficient and effective channelling;

4. Ensure that no viable project is frustrated simple for lack of funds;

5. Insulate the economy as much as possible and as much as desirable from the vicissitudes of international economic scenes; effectively sustain the indigenization (ownership, control and management) of the economy; assist in achieving significant transformation of the rural sector; and assist in achieving a greater integration and linkages in agriculture, commerce and industry.

Name: Nnamani, Great Ogomuegbunam

Reg No: 2017/249532

Department: Economics

Email: nnamanigreat20@gmail.com

The financial system establishes a network of financial institutions, markets, instruments and services to

facilitate

the transfer of funds. Intermediaries, instruments and the ultimate user of funds are the key players in the system. Since

the financial system plays a key role in the economy, it’s state is a major determining factor of the rate of economic growth.

An efficient financial system and sustainable economic growth are corrolate. The financial system mobilizes the savings

and channelizes them into the productive activity

and thus influences the pace of economic development. Economic growth is hampered for want of effective financial system. Broadly speaking,

financial system deals with three inter-related and interdependent variables, i.e., money, credit and finance.

The financial system provides channels to transfer funds from individual and groups who have saved money to individuals and group who want

to borrow money. Saver (refer to the lender) are suppliers of funds to borrowers in return with promises of repayment of even more funds in

the future. Borrowers are demanders of funds for consumer durables, house, or business plant and equipment, promising to repay borrower funds

based on their expectation of having higher incomes in the future. These promises are financial liabilities for the borrower-that is, both a

source of funds and a claim against the borrower’s future income.

Functions of the financial system include, but are not limite to:

The financial system works effectively in a bid to ensure optimum allocation of financial resources in an economy through the mechanism of establishing a link between the savers and the investors.

The system equally fosters asset-liability transformation. This occur when banks create claims (liabilities) against themselves though accepting deposits

from customers, and when they also create assets through providing loans to clients.

Secondly, economic resources (i.e., funds) are transferred from one party to another through financial system.

The financial system ensures the efficient functioning of the payment mechanism in an economy. All transactions between the buyers and

sellers of goods and services are effected smoothly because of financial system. Those who have deficit funds, through the financial system, receive funds from those who have surplus.

It is also a key role of the financial system to help in risk transformation by diversification, as in case of mutual funds. As a result of the existence of mutual funds, risks are diversified

using different benchmarks. Because risks are diversified, trust may be regained in the financial system.

Additionall, through the interaction of buyers and sellers, the financial system helps in the price discovery of financial assets. For example, the prices

of securities are determined by demand and supply forces in the capital market.

As is described above, the financial market plays a significant role in economic growth through the competent allocation of capital, monitoring managers,

mobilizing of savings and promoting technological changes among others. It is, therefoe, pertinent that the financial sector of every economy is developed and wee managed in order stimulate

economic growth.

A financial institution (FI) is a company engaged in the business of dealing with financial and monetary transactions such as deposits, loans, investments, and currency exchange. … Virtually everyone living in a developed economy has an ongoing or at least periodic need for the services of financial institutions.

Financial Institutions are referred to as a company that deals in all types of finance-related businesses. They are different from banks and play a very important part in broadening the financial services in the country. They provide a very attractive rate of returns to the customers in comparison to any government-centric banks. It deals in loans and advances and also specializes in some specified sectors like hire purchases and leasing etc.

Explanation

The financial institution deals with finance-related services. These are gaining popularity day by day nowadays. The attractive rate of returns on the customer’s investment is very demanding. It also provides specialized services like hire purchase and leasing, etc. The simple and organized procedure of the institutions is becoming very complementary. It provide a broad range of business opportunities. There are different types of financial institutions. The goal of all the institutions is different and they provide different services and have different levels of risk associated with it. All the financial institutions have unique features and it works in a specialized way. The financial institution is gaining immense popularity in broadening the finance-related services in the country.

Start Your Free Investment Banking Course

Download Corporate Valuation, Investment Banking, Accounting, CFA Calculator & others

Role of Financial Institutions

The financial institution provides varied kinds of financial services to the customers.

The financial institution provides an attractive rate of return to the customers.

Promotes the direct investment by the customers and making them understand the risk associated with that as well.

It helps in forming the liquidity of the stock in case of an emergency in the financial markets.

Features

It provides a high rate of return to the customers who have invested in the financial institution.

It reduces the cost of financial services provided.

It is considered very important for the development of financial services in the country.

It also advises the customers on how to deal with the equity and the other securities bought and sold in the market.

It helps to improvise decision making because it follows a systematic approach to calculate all the risks and rewards.

How does it work?

Financial institutions work like banks in some ways. They give loans and advances to the customers and also set a platform for the customers to do some investments. The customers get exciting offers and returns from them and therefore these institutions are gaining popularity. It also provide consultancy services to the clients on their investments related to the financial markets where the huge amount of risk is involved. Moreover, the customers who are handing over their hard-earned monies to such institutions should check for the history and origin of this financial institution.

Types of Financial Institutions

Investment Banks

Commercial Banks

Internet Banks

Retail Banking

Insurance companies

Mortgage companies.

Functions

The financial institutions provide loans and advances to the customers.

The rate of return is very high in case of investment made in this type of institution.

It also gives a high rated consultancy to the customers for their beneficial investments.

It also serve as a depository for their customers.

It can also make an effort to minimize the monitoring cost of the company.

All the finance related work is done by the financial institution or on behalf of the customers.

Financial Institutions vs Banks

The functions of payments of various services are done by the bank but the financial i nstitutions will not be able to do so.

It cannot accept the demand deposit whereas the banks can accept the demand deposit by the customers.

Banks provide the guarantee of repayment of the deposit whereas the financial institutions may fail to do so.

Advantages and Disadvantages

Below are the advantages and disadvantages:

Advantages

The financial institutions help in the upliftment of the economies of our country.

It has been proved to be more successful in terms of return earned by the customers since the rate of return is higher compared to any other place.

It is also a smart way to invest money and keep the money rotated in the finance market.

It provides financial services to the customers.

The repayment facility is also very well managed in the financial institutions.

It also provide underwriting facilities.

Disadvantages

The process is very complex for some customers because they try to indulge in various businesses and end up making confusion for themselves.

In case of default done by the management of the financial institutions, the customers will have to face major worse circumstances. The money which they have invested may not be recovered. Sometimes the principal amount is not assured to be recovered because the government in case of default announces a certain sum of money which will be repaid and most of the time the amount of government declare to be repaid is very less in comparison to the principal amount of the investment made.

In addition to the meaning of financial system,A ‘Financial system’ is a system that allows the exchange of funds between financial market participant such as lenders, investors, and borrowers. Financial systems operate at national and global levels.Financial Institutions consist of complex, closely related services, markets, and institutions intended to provide an efficient and regular linkage between investors and depositors.

In other words, financial systems can be known wherever there exists the exchange of a financial medium (money) while there is a reallocation of funds into needy areas (financial markets, business firms, banks) to utilize the potential of ideal money and place it in use to get benefits out of it. This whole mechanism is known as a financial system.

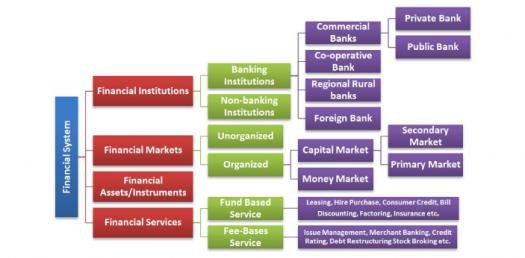

COMPONENTS OF FINANCIAL SYSTEM

Financial system provide financial services for members and clients. It is also termed as financial intermediaries because they act as middlemen between the savers and borrowers. There are mainly four components of the financial system:

Financial markets

Financial assets

Financial institutions

Financial services

1. Financial markets – the market place where buyers and sellers interact with each other and participate in the trading of bonds, shares and other assets are called financial markets.

2. Financial assets – the products which are traded in the financial markets are called financial assets. Based on different requirements and credit seekers, the securities in the market also differ from each others.

3. Financial institutions – financial institutions are acting as a mediator between the investors and borrowers. The investor’s savings are mobilized either directly or indirectly via the financial markets. They offer services to organisations who want to raise funds from markets and take care of financial assets (deposits, securities, loan, etc).

4. Financial services – services provided by assets management and liabilities management companies. They help to get the required funds and also make sure that they are efficiently invested. (eg. banking services, insurance services and investment services)

NAME: OKOYE OBINNA CHIDIEBERE

REG NO: 2014/191864

The Financial System

A financial system is a system put in place to bridge the gap between lenders and borrower. It is a densely interconnected network of intermediaries, facilitators, and markets that serves three major purposes: allocating capital, sharing risks, and facilitating all types of trade, including intertemporal exchange. The Financial System is made up of three units and they are: Financial Institutions (the banks and other), Financial Markets (the money and capital markets), and Financial Instruments (Cash instruments as well as securities). Some scholars may believe that the financial system supports the life-blood of the economy because it allows for the movement of money from areas of surplus funds to areas of deficit, thus allowing for the financing of investments that lead to the overall economic development of the economy.

ROLES OF FINANCIAL INSTITUTIONS

1. The financial systems offer a very convenient mode of payment for goods and services. The check system, credit card systems and others are the easiest methods of payment in the economy; they also drastically reduce the cost and rime of transactions.

2. Most governments intervene in the financial system to influence macroeconomic variables like interest rates or inflation. For example, the federal bank or a central bank does indulge in several cuts in CRR and try to force the interest rates down and increase the availability of credit-at cheaper rates to the corporates.

3. As already stated, public savings find their way into the hands of those in production through the financial system. Financial claims are issued in the money and capital markets, which promise future income flows. The funds, in the hands of the producers, resulting in the production of better goods and services and an increase in society’s living standards. When savings flow decline, however, the growth of investment and living standards begins to fall.

4. Money in the form of deposits offers the least risk of all financial instruments. But its value mostly eroded by inflation. That is why one always prefers to store funds in financial instruments like stocks, bonds, debentures, etc. However, in such investments a greater level of risk is involved, and the degree of liquidity (i.e., conversion of the claims into money) is less. The financial markets provide the investor with the opportunity to liquidate the investments.

NAME:OKEKE OGADIMMA NANCY

REG NO:2017/249557

EMAIL:ogadimmanancy12@gmail.com

A financial system is a set of institutions, such as banks, insurance companies, and stock exchanges that permit the exchange of funds and with the aid financial markets (such as those that trade stocks or bonds), instruments (from bank CDs to futures and derivatives), and institutions (from banks to insurance companies to mutual funds and pension funds) provide opportunities for investors to specialize in particular markets or services, diversify risks, or both.

Financial systems exist on firm, regional, and global levels. Borrowers, lenders, and investors exchange current funds to finance projects, either for consumption or productive investments, and to pursue a return on their financial assets.

The financial system also includes sets of rules and practices that borrowers and lenders use to decide which projects get financed, who finances projects, and terms of financial deals.

Economic development of any country depends on the infrastructure facility available in the country. In the absence of key industries like coal, power and oil, development of other industries will be hampered. It is here that the financial services play a crucial role by providing funds for the growth of infrastructure industries.

Private sector will find it difficult to raise the huge capital needed for setting up infrastructure industries. For a long time, infrastructure industries were started only by the government in India. But now, with the policy of economic liberalization, more private sector industries have come forward to start infrastructure industry. The Development Banks and the Merchant banks help in raising capital for these industries.

The financial system helps in the promotion of both domestic and foreign trade. The financial institutions finance traders and the financial market helps in discounting financial instruments such as bills. Foreign trade is promoted due to per-shipment and post-shipment finance by commercial banks. They also issue Letter of Credit in favor of the importer. Thus, the precious foreign exchange is earned by the country because of the presence of financial system.

The best part of the financial system is that the seller or the buyer do not meet each other and the documents are negotiated through the bank. In this manner, the financial system not only helps the traders but also various financial institutions. Some of the capital goods are sold through hire purchase and installments system, both in the domestic and foreign trade. As a result of all these, the growth of the country is speeded up.

The successful expansion of any Economy is dependent on the strength of it’s financial system. This implies that the stronger the financial system, the bigger and better the Economy and vice versa. The financial system through the link it creates between savings and investment, boosts the creation of wealth in the country. It also assists in the supply of necessary financial inputs for the production of goods and services, in turn, promote the well-being and standard of living of people in the country.

However, the financial system through the role it performs can go a long way to promote Economic growth and development. It can do this by acting as an intermediary between lenders and borrowers, thus the various sectors in the Economy most especially the businesses and industries, will get the finances they need, this will automatically lead to increased productivity, increase in the level of employment, enhanced domestic trade and increase in economic activities and so on.

Thus they enhance the efficiency of investment and this leads to higher Economic growth and development. Moreover, they also raise funds for both short-term and long-term money requirements. They help the government create policies that will stabilize the Economy in case there was an Economic disequilibrium. All these help to create Economic development.

Agbo Jennifer Amarachi

2017/249476

jenniferamarachi.agbo@gmail.com

https://agbojenniferamarachi.blogspot.com/?m=1

The successful expansion of any Economy is dependent on the strength of it’s financial system. This implies that the stronger the financial system, the bigger and better the Economy and vice versa. The financial system through the link it creates between savings and investment, boosts the creation of wealth in the country. It also assists in the supply of necessary financial inputs for the production of goods and services, in turn, promote the well-being and standard of living of people in the country.

However, the financial system through the role it performs can go a long way to promote Economic growth and development. It can do this by acting as an intermediary between lenders and borrowers, thus the various sectors in the Economy most especially the businesses and industries, will get the finances they need, this will automatically lead to increased productivity, increase in the level of employment, enhanced domestic trade and increase in economic activities and so on.

Thus they enhance the efficiency of investment and this leads to higher Economic growth and development. Moreover, they also raise funds for both short-term and long-term money requirements. They help the government create policies that will stabilize the Economy in case there was an Economic disequilibrium. All these help to create Economic development.

Agbo Jennifer Amarachi

2017/249476

jenniferamarachi.agbo@gmail.com

https://agbojenniferamarachi.blogspot.com/?m=1

The successful expansion of any Economy is dependent on the strength of it’s financial system. This implies that the stronger the financial system, the bigger and better the Economy and vice versa. The financial system through the link it creates between savings and investment, boosts the creation of wealth in the country. It also assists in the supply of necessary financial inputs for the production of goods and services, in turn, promote the well-being and standard of living of people in the country.

However, the financial system through the role it performs can go a long way to promote Economic growth and development. It can do this by acting as an intermediary between lenders and borrowers, thus the various sectors in the Economy most especially the businesses and industries, will get the finances they need, this will automatically lead to increased productivity, increase in the level of employment, enhanced domestic trade and increase in economic activities and so on.

Thus they enhance the efficiency of investment and this leads to higher Economic growth and development. Moreover, they also raise funds for both short-term and long-term money requirements. They help the government create policies that will stabilize the Economy in case there was an Economic disequilibrium. All these help to create Economic development.

Name: Ugorji Ijeoma Judith

Reg no: 2017/243088

Department: Economic

Blog: peppyxperience.blogspot.com

Email: peppyhijay@gmail.com

The financial system and it’s role in economic development.

The financial system is a broad concept that encompasses the interactions and interrelationships of various financial units, groups and institutions of an economy for the purpose of expansion, growth and development. It is a fundamental, well organized and regulated economic structure upon which the financial activities/ affairs of an economy rest on. No economic entity can operate without finance. There cannot be any productive activity in any economy with funds and capital, hence the indispensable need of a financial system.

The economic growth of any country largely depends upon the existence of a well ordered financial system. The financial system can be likened to the circulatory system of the body which circulates blood to the various organs of the body in other to ensure proper functioning of all organs so also the financial system circulates funds to the various components of the economy to keep active the productive activities of the economy. It is a mechanism that channels funds from the surplus economic unit( those who have funds and not in use of it) tobthw deficit economic unit( those who do not have fund but have need of it for the purpose of investment and production). The surplus economic unit are the households/individuals who are the owners of resources, factors of production. The deficit unit are fund seekers. They are mainly the business firms and government.

As mentioned earlier, the financial system is an interrelation of various components. These components are called financial intermediaries who play the role of bringing bringing borrowers and lenders in an economy together by transferring funds from area of surplus (lenders) to area of deficit (borrowers). Examples of financial intermediaries are Banks, Insurance companies, Depositories, mortgage house etc. Each of these intermediaries have specific roles they play in the economy. They operate under a market known as the financial market. The financial market is an arrangement where financial items of value are sold and bought. These finance items include but not limited to shares, bonds, securities, equity and currency.

Important roles of the financial system in an economy

Having mentioned that the expansion of every economy largely depends on a financial system, it’s importance therefore cannot be overemphasized. The various fuctions of the financial system are outlined below.

A fundamentally important role of the financial system in an economy is the channeling of funds from the surplus economic units to the deficit economic units for productive activities to take place.

A financial system plays a vital role in economic growth and development through provision of funds/capital for investment. Increase in investment leads to a substantial increase in employment which in turn leads to increase in income.

The financial system ensures efficient and effective allocation and uses of capital and other resources.

The financial system encourages innovation and invention by creating new and better ways of transaction at very low cost.

It encourages international trade by making provision for buying and selling of different currencies at a given exchange rate. This also leads to expansion in business frontiers.

A well ordered and organised financial system provides yardstick for government in deciding and implementing monetary policies.

Udeh Rita Ezinne

2017/249578

ritaudeh563@gmail.com

A country can be said to be a country when there is an existence of financial system

The financial system includes all financial intermediaries that operate in the financial sector in the economy. It is termed as financial intermediaries because they act as middlemen between the savers and borrowers.

It is anchored on the belief that economic agents are categorized into surplus and deficit spending units. The surplus spending units are individuals, groups or organizations operating within the economy that have excess funds above their immediate needs. They constitute suppliers of surplus funds to the financial system. The deficit spending units are those that have a shortage of funds and thus require borrowing to fund their operations. They are the users of the excess funds supplied by the surplus spending units in the financial system.With intermediation, savers lend to intermediaries, who in turn lend firms and other fund using units. The saver holds claim against the intermediaries, in form of deposits rather than against the firm. These institutions provide a useful service by reducing the cost to individuals, of negotiating transactions, providing information, achieving

There are mainly four components of the financial system:

1. Financial markets – the market place where buyers and sellers interact with each other and participate in the trading of bonds, shares and other assets are called financial markets.

2. Financial assets – the products which are traded in the financial markets are called financial assets. Based on different requirements and credit seekers, the securities in the market also differ from each others.

3. Financial institutions – financial institutions are acting as a mediator between the investors and borrowers. The investor’s savings are mobilized either directly or indirectly via the financial markets. They offer services to organisations who want to raise funds from markets and take care of financial assets (deposits, securities, loan, etc).

4. Financial services – services provided by assets management and liabilities management companies. They help to get the required funds and also make sure that they are efficiently invested. (eg. Banking services, insurance services and investment services)

Conclusion

The financial system provides an enabling environment for economic Growth and development, productive activity, financial Intermediation, capital formation and management of the payments System.

NAME: IJE VORDA GOODNESS

REG NO: 2017/249514

EMAIL: vordagoodness78@gmail.com

ECO 324

ANSWERS

Borrowers or deficit unit of the economy don’t know the net savers.

Borrowers or deficit unit of the economy don’t know the net savers.

Those with excess funds may lack trust in the investors. Since customers trust the financial intermediaries, they keep their idle funds with them, the financial intermediaries promise net savers to pay them whenever they need the money. This function is called savings mobilization.

Those with excess funds may lack trust in the investors. Since customers trust the financial intermediaries, they keep their idle funds with them, the financial intermediaries promise net savers to pay them whenever they need the money. This function is called savings mobilization.

The amount required by an investor may be too much for a saver or few savers to provide. Since financial institutions have access to the funds of numerous savers pooled together they lend to investors on behalf of net savers.

The amount required by an investor may be too much for a saver or few savers to provide. Since financial institutions have access to the funds of numerous savers pooled together they lend to investors on behalf of net savers.

Financial institutions perform the function of financial intermediation. This is done because there are participants in the financial market who have access to excess money and they don’t want to consume now i.e net savers and deficit participants who are in immediate need of excess funds for investment i.e net borrowers. Financial institutions therefore helps in the transfer of these funds from the net savers to the net borrowers.

Without financial institution the role of financial intermediation will be impossible since

Now it’s imperative to note that this funds are lended to investors on an interest rate which they use to generate extra credit in the economy and boost economic growth. They also give a part of the interest to the net savers to encourage them to save more of their excess funds. Before investors are given loans their business plans are scrutinized for profitability and positive impacts that the economy will get from lending such loans.

The loan given to these investors help in generating employment and productivity which leads to increase in the level of income and output (GDP).

Moreover financial institutions carry out the monetary policies of the government that help in stabilizing the economy.

Name: Ani Gabriel ogbonna

Reg. Number: 2017/249483

Department: Economics

Email: anigabriel05@gmail.com

FINANCIAL SYSTEM

A financial system is a set of institutions, such as banks, insurance companies, and stock exchanges, that permit the exchange of funds. Financial systems exist on firm, regional, and global levels. Borrowers, lenders, and investors exchange current funds to finance projects, either for consumption or productive investments, and to pursue a return on their financial assets. The financial system also includes sets of rules and practices that borrowers and lenders use to decide which projects get financed, who finances projects, and terms of financial deals. Financial systems can be organized using market principles, central planning, or a hybrid of both. Institutions within a financial system include everything from banks to stock exchanges and government treasuries.

The Financial system is one of the most important inventories of modern society. The phenomenon of imbalance in the distribution of capital or funds exists in every economic system. There are areas or people with surplus funds, while other areas or people are facing a deficit. A financial system functions as an intermediary and facilitates the flow of funds from the areas of surplus to the areas of deficit. It is a composition of various institutions, markets, regulations and laws, practices, money managers, analysts, transactions, and claims & liabilities.

The financial system helps determine both the cost and the volume of credit. This system can affect a rise in the cost of funds, thus adversely affecting the consumption, production, employment, and growth of the economy. Vice-versa, lowering the cost of credit can have a positive effect and enhance all the above factors. Clearly, a financial system has an impact on the basic existence of an economy and its citizens.

Financial system perform different function in the society. This function aid in development of Economy.

1. The Savings Function:

As already stated, public savings find their way into the hands of those in production through the financial system. Financial claims are issued in the money and capital markets, which promise future income flows. The funds, in the hands of the producers, resulting in the production of better goods and services and an increase in society’s living standards. When savings flow decline, however, the growth of investment and living standards begins to fall.

2. Liquidity Function:

Money in the form of deposits offers the least risk of all financial instruments. But its value mostly eroded by inflation. That is why one always prefers to store funds in financial instruments like stocks, bonds, debentures, etc. However, in such investments (i) a greater level of risk is involved, (ii) and the degree of liquidity (i.e., conversion of the claims into money) is less. The financial markets provide the investor with the opportunity to liquidate the investments.

3. Payment Function.

The financial systems offer a very convenient mode of payment for goods and services. The check system, credit card systems et al are the easiest methods of payment in the economy; they also drastically reduce the cost and rime of transactions.

4. Risk Function:

The financial markets provide protection against life, health, and income risks. These are accomplished through the sale of life, health, and property insurance policies. Overall, they provide immense opportunities for the investor to hedge himself/herself against or reduce the possible risk involved in various instruments.

5. Policy Function:

Most governments intervene in the financial system to influence macroeconomic variables like interest rates or inflation. For example, the federal bank or a central bank does indulge in several cuts in CRR and try to force the interest rates down and increase the availability of credit-at cheaper rates to the corporates.

Conclusion:

Modern-day economies require huge sums of money for investment in capital assets (land, types of equipment, factory, etc.), which are then used for providing goods and services. The funds required are so huge that it’s not possible for a single government/firm to meet the requirement. By selling financial claims like stocks, bonds, etc., the required funds can be quickly raised from a variety of investors. The business firm/government issuing such a financial claim then hopes to return the borrowed funds from expected future inflows. Indeed, we see that the financial markets within the financial system have made possible the exchange of current income for future income and transformation of savings into investments so that production and income keep growing and there by bringing economic development.

Name:Oroke Charity Nnedimma

Reg no:2017/243816

E-mail address: amieeukpaka@gmail.com

Department:Economics

Course code: Eco 361

Harris–Todaro migration model

The Harris–Todaro model, named after John R. Harris and Michael Todaro, is an economic model developed in 1970 and used in development economics and welfare economics to explain some of the issues concerning rural-urban migration. The main assumption of the model is that the migration decision is based on expected income differentials between rural and urban areas rather than just wage differentials. This implies that rural-urban migration in a context of high urban unemployment can be economically rational if expected urban income exceeds expected rural income.

.GENERAL ASSUMPTIONS OF THE MODEL

Two sectors: urban (manufacture) and rural (agriculture)

Rural-urban migration condition: when urban real wage exceeds real agricultural product

No migration cost

Perfect competition

Cobb-Douglas production function

Static approach

Low risk aversion

Overview of the model

In the model, an equilibrium is reached when the expected wage in urban areas (actual wage adjusted for the unemployment rate), is equal to the marginal product of an agricultural worker. The model assumes that unemployment is non-existent in the rural agricultural sector. It is also assumed that rural agricultural production and the subsequent labor market is perfectly competitive. As a result, the agricultural rural wage is equal to agricultural marginal productivity. In equilibrium, the rural to urban migration rate will be zero since the expected rural income equals the expected urban income. However, in this equilibrium there will be positive unemployment in the urban sector. This model can be used to explains internal migration in Nigeria as the regional income gap has been proved to be a primary drive of rural-urban migration, while urban unemployment is local governments’ main concern in many cities.

CONCLUSION

Harris Todaro model explains some issues of rural-urban migration. This migration happens in case when expected rural income is higher than rural wages. In this case economy may have high rates of unemployment. The equilibrium condition of this model is when expected rural wage is equal to rural wage. When government subsidize manufacturing sector Harris Todaro paradox may happen.

According to the authors job creation instead of dealing with unemployment problem actually may cause increase of unemployment. This happens when urban-rural wage differential is high enough, so rural workers move to the cities hoping to find a job with high wage. Obviously, not

all these workers succeed in finding jobs which leads to unemployment. Another issue is that inducing minimum wages creates labor market distortions. Therefore, policy makers should not set the minimum wage rates. In addition, simulations showed that different policies’ outcomes depend on elasticity of labor demand in different sectors and on marginal product of labor. As Harris and Todaro suggested the first-best policy would be subsidizing manufacturing

Lewis Ranis-Fei Growth model

Fei–Ranis model of economic growth is a dualism model in developmental economics or welfare economics that has been developed by John C. H. Fei and Gustav Ranis and can be understood as an extension of the Lewis model. It is also known as the Surplus Labor model. It recognizes the presence of a dual economy comprising both the modern and the primitive sector and takes the economic situation of unemployment and underemployment of resources into account, unlike many other growth models that consider underdeveloped countries to be homogenous in nature. According to this theory, the primitive sector consists of the existing agricultural sector in the economy, and the modern sector is the rapidly emerging but small industrial sector. Both the sectors co-exist in the economy, wherein lies the crux of the development problem. Development can be brought about only by a complete shift in the focal point of progress from the agricultural to the industrial economy, such that there is augmentation of industrial output. This is done by transfer of labor from the agricultural sector to the industrial one, showing that underdeveloped countries do not suffer from constraints of labor supply. At the same time, growth in the agricultural sector must not be negligible and its output should be sufficient to support the whole economy with food and raw materials. Like in the Harrod–Domar model, saving and investment become the driving forces when it comes to economic development of underdeveloped countries

The three fundamental ideas used in this model are:

Agricultural growth and industrial growth are both equally important;

Agricultural growth and industrial growth are balanced;

Only if the rate at which labor is shifted from the agricultural to the industrial sector is greater than the rate of growth of population will the economy be able to lift itself up from the Malthusian population .

Connectivity between sectors

Fei and Ranis emphasized strongly on the industry-agriculture interdependency and said that a robust connectivity between the two would encourage and speedup development. If agricultural laborers look for industrial employment, and industrialists employ more workers by use of larger capital good stock and labor-intensive technology, this connectivity can work between the industrial and agricultural sector. Also, if the surplus owner invests in that section of industrial sector that is close to soil and is in known surroundings, he will most probably choose that productivity out of which future savings can be channelized. They took the example of Japan’s dualistic economy in the 19th century and said that connectivity between the two sectors of Japan was heightened due to the presence of a decentralized rural industry which was often linked to urban production. According to them, economic progress is achieved in dualistic economies of underdeveloped countries through the work of a small number of entrepreneurs who have access to land and decision-making powers and use industrial capital and consumer goods for agricultural practices.

A significant conclusion of the Lewis-Ranis-Fei model. In effect, a shift in the terms of trade has a negative effect on the industry, forcing capitalist employers to pay a higher wage and thus generating less profits and less investment (Berry, 1970). However, there is a role of interdependence between the two sectors (Ranis and Fei). In fact, raising the price of goods in agriculture would give an agricultural sector an incentive to raise the output, thus encouraging investments in agriculture, leading to a decline in the terms of trade, which in turn lowers wages, increases profits and generates more investment in the industry. Consequently, there will be a balanced expansion in both, agriculture and industry. In other words, what Ranis and Fei observed was that the allocation of investment funds must be such that as to “continuously sustain investment incentives in both sectors of the economy”.

the main ideas behind the Lewis-Ranis-Fei model has been explained above and used consecutive for analysis of the model to explain why it is important to invest in both sectors in order to remain on the balanced growth path and maintain the rate of industrialization. The existence of surplus labour in agriculture allows the industry to continue to pay the institutional wage and therefore enjoy further profits and continued investment. At the same time, as more and more people are moving away from agriculture, there will be some amount of u agricultural surplus that can be used up to fuel further development. This process continues until the surplus labour is absorbed. Hence, saving and investment are a crucial part in the Lewis-Ranis-Fei to support economic development.

Name : Oroke Charity Nnedimma

Reg No: 2017/243816

Department: Economics

Course code: 324

Financial markets involve various players, including borrowers, lenders, and investors that negotiate loans for investment purposes. The borrowers and lenders tend to trade money in exchange for a return on the investment at some future date. Derivative instruments are also traded in the financial markets as well, which are contracts that are determined based on an underlying asset’s performance.

Financial system in Nigeria is regulatory based and has been described as a complicated sectors since it handles the economy, cash flow, financial commitment as well as other finance releated subject. The operators of nigeria financial system are the major players in the industry, the financial system in Nigeria is controlled by various department and agencies of the federal government which are empowered to regulate the formation and operations of financial intermediaries and other operators in the system.

The structure of financial system in Nigeria was designed in a way that the control agencies also determine which financial instruments could be traded and at what rates. They help to monitor the entire system. The Nigerian financial system regulators has the task of controlling and managing the system rests primarily on the federal ministry of finance. The ministry plays a dual role.

Nigeria has enabled the operators of Nigeria financial system to be the financial managers and also the controllers whose function is operationally carried out by the central bank of Nigeria (CBN). Until recently, the bank was under the ministry but has now gained a large measure of autonomy and has been placed directly under the presidency. The central bank exerts a lot of influence on the financial system. Its influence is most pervasive on the banking subsector. It acts as the controller and regulator of the financial system. One medium through which the central bank of Nigeria exercise its control is the monetary policy circulars (MPC) issued from time to time by the bank.

Components of Financial System

Financial Institutions

Financial Markets

Financial Instruments (Assets or Securities)

Financial Services

Money

Financial institutions facilitate smooth working of the financial system by making investors and borrowers meet. They mobilize the savings of investors either directly or indirectly via financial markets, by making use of different financial instruments as well as in the process using the services of numerous financial services providers

Financial Markets

A financial market is the place where financial assets are created or transferred. It can be broadly categorized into money markets and capital markets. Money market handles short-term financial assets (less than a year) whereas capital markets take care of those financial assets that have maturity period of more than a year. The key functions are:

1. Assist in creation and allocation of credit and liquidity.

2. Serve as intermediaries for mobilization of savings.

3. Help achieve balanced economic growth.

4. Offer financial convenience

Financial Instruments

This is an important component of financial system. The products which are traded in a financial market are financial assets, securities or other type of financial instruments. There is a wide range of securities in the markets since the needs of investors and credit seekers are different. They indicate a claim on the settlement of principal down the road or payment of a regular amount by means of interest or dividend. Equity shares, debentures, bonds, etc are some examples.

Financial Services

Financial services consist of services provided by Asset Management and Liability Management Companies. They help to get the necessary funds and also make sure that they are efficiently deployed.

Money

Money is understood to be anything that is accepted for payment of products and services or for the repayment of debt. It is a medium of exchange and acts as a store of value.

Meaning of Financial Assets

Financial assets are not existed in physical form.

These assets represent the ownership right in a piece of paper.

Characteristics of financial Asset

Divisibility & Denomination